Property Markets Under Pressure: Why Uncertainty Is Weighing on New Zealand Housing

Squirrel’s Chief Operating Officer Dave Tyrer explains why recent volatility is stalling New Zealand’s housing recovery – and why income focused investors may still find opportunity as interest rates rise.

A Cautious Start to March for Property Markets

- After seeing early signs of recovery in late 2025 / early 2026, weakness has returned to New Zealand’s housing market.

- Global uncertainty is the big factor impacting demand—as the Middle East crisis and climbing oil prices add to cost-of-living pressures, causing concern around the future of inflation and the potential for rising interest rates.

- House prices are expected to track sideways in 2026, but with OCR hikes expected this year, there’s an opportunity for Squirrel Monthly Income Fund investors to ride interest rates upwards.

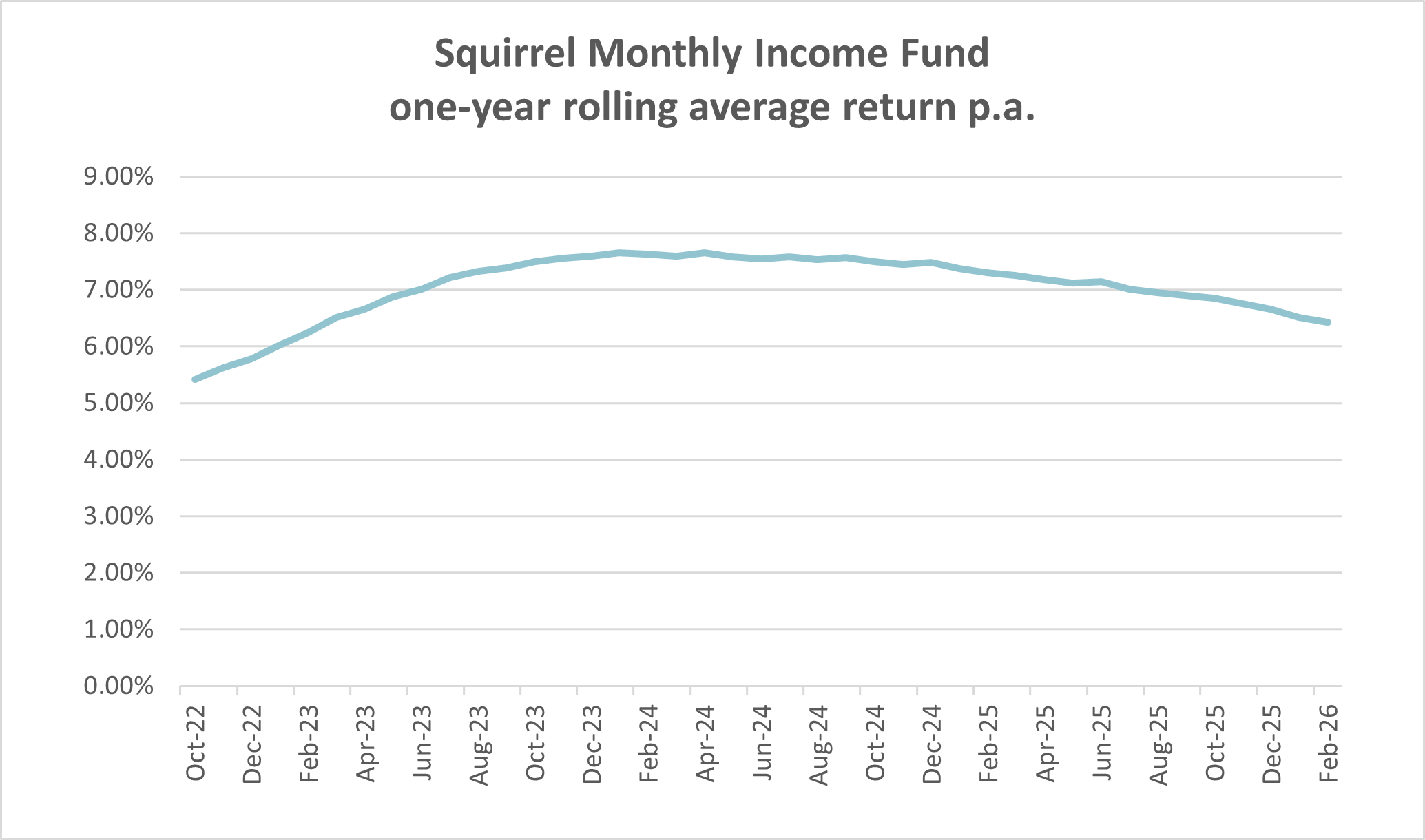

- Squirrel’s Monthly Income Fund invests in loans secured by first mortgages over residential property, and over the 12 months to 31 March 2026 has generated returns of 6.36% p.a. (peaking at 7.65% p.a. at the highs of the last interest rate cycle).*

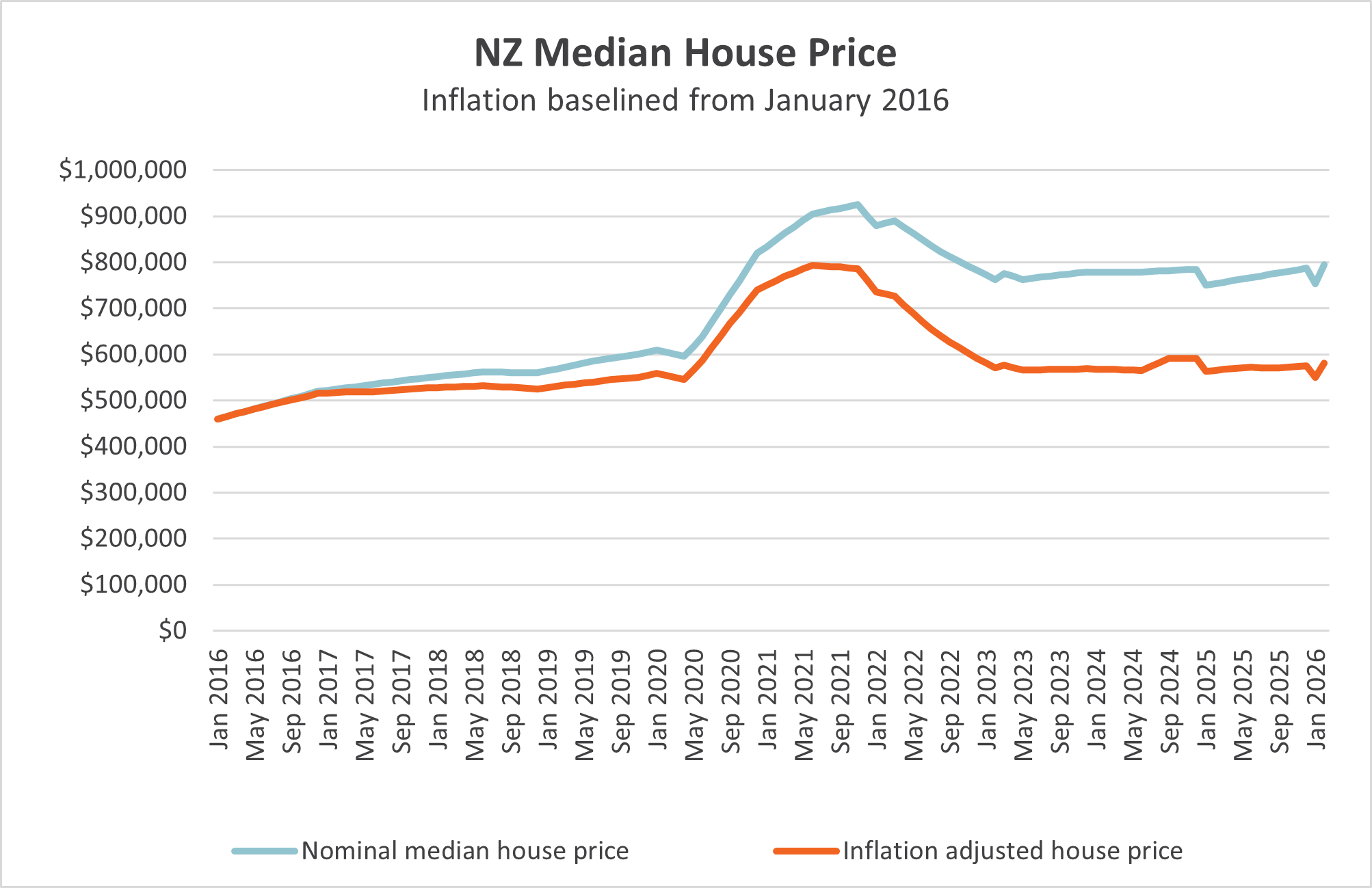

Go back five years, and New Zealand’s residential property market was on a bubble run.

With interest rates at historic lows, asset prices rose rapidly. Data from QV estimates national average house prices climbed by nearly 30% during 2021.

But the bubble had to burst. Since the market correction, nominal house prices have largely traded sideways. Once you factor inflation into the equation, prices have remained largely unchanged since 2020.

Source: REINZ & Statistics NZ

Following an extended period of weakness, sales numbers finally started to pick up again late last year, and into early 2026—although it was still by no means a period of high demand.

But any signs of a recovery have dropped away with the commencement of the US-Iran conflict in the Middle East.

Local, on-the-ground reports from the last month suggest open home traffic is down; mortgage application numbers have dropped; and as of early April, cost increases are starting to flow through to the construction sector as well.

Unsurprisingly, it’s uncertainty which is pulling demand back—driven by things like:

- Interest rates have now started to rise, with the markets anticipating higher levels of inflation thanks to surging oil prices.

- Cost of living pressures (both real and expected)

- And concerns around employment prospects.

More broadly, the unpredictability that comes with an election year is also having an impact.

History shows that people typically don’t like to commit to big purchases in the lead-up to an election—and anecdotal feedback (from property investors in particular) suggests they’re holding off, watching and waiting to see how things play out.

Across the four big drivers that typically underpin housing market performance—supply, demand, confidence, and access to credit—there’s further signs of weakness.

- Supply of new homes remains high, and we’re still seeing high levels of stock / listings in the market.

- Net immigration remains muted—and is likely to stay that way until the economy is more firmly on the road to recovery.

- The counterargument to this being that, with the global situation as volatile as it is, more people may opt to stick around in NZ rather than travel / move overseas.

- Jobs and economic confidence remain soft

- On the plus side, credit conditions are positive i.e. lenders are lending

The outlook on house prices

In short, the conditions just aren’t there to support a recovery in either house prices or sales volumes—so we’re likely in for another year of house prices continuing to slide sideways in nominal terms, and probably backwards in inflation-adjusted terms.

The possible exception (and one part of the housing market I’ll be watching with interest) is the $4 million+ segment.

Since Government launched its new “Golden Visa” in early March (the one requiring visa holders to build or purchase a $5m+ home) over 650 applications have been received.

Right now, there are between 3,500 – 5000 homes worth more than $5m in NZ, tightly concentrated in Auckland and Queenstown. Around 600 of those are currently listed for sale.

There will be an increase in demand in this price bracket, which could potentially see some ‘under $5m’ homes suddenly become $5m+.

Are flat house prices a bad thing?

Over the last 35 years or so, New Zealand’s economic growth has been heavily reliant on house prices tracking upwards, and that’ll be a tough habit to break.

But taking a generational view, flat house prices are arguably a good thing for people living and working in New Zealand.

Implications for investor returns

Squirrel’s Monthly Income Fund invests in loans secured by first mortgages over residential property.

The loans tend to be shorter term (less than three years) meaning the bulk of our current loan portfolio was written after house prices fell. The benefit of this is that the security for the lending is in good shape, and borrowers continue to meet their commitments.

The Squirrel Monthly Income Fund has returned 6.36%* over the last 12 months (to 31 March 2026).

Over the last interest rate cycle, the Fund returns peaked around 7.65%* p.a., giving investors a sense of the range of returns that could be expected from the Fund over time.

Based on its 8 April Monetary Policy Review, the RBNZ is expecting to deliver OCR increases starting later this year, which will flow through to retail interest rates.

The timeframe for that will be heavily dependent on how quickly the Middle East crisis and resulting oil shortages get resolved—and to what degree rising oil prices flow through to increased inflation in the economy.

That means we could see an increase to the return for investors later in the year given the loans made by the Fund have variable interest rates.

The Monthly Income Fund is a moderate risk investment aiming to deliver strong capital protection and makes monthly distributions.

So, despite ongoing weakness in the residential property market, the Fund continues to find good quality loans to invest into.

If you’re looking to keep your investments local – and hoping to ride interest rates upwards over the next few years – Squirrel’s Monthly Income Fund could be a good option to consider for the conservative to moderate risk part of your portfolio.

* Returns are net of fees and expenses and before tax.

For further information on the Squirrel Income Fund, including a copy of the Product Disclosure Statement, and to read other opinions and commentary pieces from Dave and the team at Squirrel, please visit Squirrel Landing Page on InvestNow.

Property Markets Under Pressure: Why Uncertainty Is Weighing on New Zealand Housing

Squirrel’s Chief Operating Officer Dave Tyrer explains why recent volatility is stalling New Zealand’s housing recovery – and why income focused investors may still find opportunity as interest rates rise.

A Cautious Start to March for Property Markets

- After seeing early signs of recovery in late 2025 / early 2026, weakness has returned to New Zealand’s housing market.

- Global uncertainty is the big factor impacting demand—as the Middle East crisis and climbing oil prices add to cost-of-living pressures, causing concern around the future of inflation and the potential for rising interest rates.

- House prices are expected to track sideways in 2026, but with OCR hikes expected this year, there’s an opportunity for Squirrel Monthly Income Fund investors to ride interest rates upwards.

- Squirrel’s Monthly Income Fund invests in loans secured by first mortgages over residential property, and over the 12 months to 31 March 2026 has generated returns of 6.36% p.a. (peaking at 7.65% p.a. at the highs of the last interest rate cycle).*

Go back five years, and New Zealand’s residential property market was on a bubble run.

With interest rates at historic lows, asset prices rose rapidly. Data from QV estimates national average house prices climbed by nearly 30% during 2021.

But the bubble had to burst. Since the market correction, nominal house prices have largely traded sideways. Once you factor inflation into the equation, prices have remained largely unchanged since 2020.

Source: REINZ & Statistics NZ

Following an extended period of weakness, sales numbers finally started to pick up again late last year, and into early 2026—although it was still by no means a period of high demand.

But any signs of a recovery have dropped away with the commencement of the US-Iran conflict in the Middle East.

Local, on-the-ground reports from the last month suggest open home traffic is down; mortgage application numbers have dropped; and as of early April, cost increases are starting to flow through to the construction sector as well.

Unsurprisingly, it’s uncertainty which is pulling demand back—driven by things like:

- Interest rates have now started to rise, with the markets anticipating higher levels of inflation thanks to surging oil prices.

- Cost of living pressures (both real and expected)

- And concerns around employment prospects.

More broadly, the unpredictability that comes with an election year is also having an impact.

History shows that people typically don’t like to commit to big purchases in the lead-up to an election—and anecdotal feedback (from property investors in particular) suggests they’re holding off, watching and waiting to see how things play out.

Across the four big drivers that typically underpin housing market performance—supply, demand, confidence, and access to credit—there’s further signs of weakness.

- Supply of new homes remains high, and we’re still seeing high levels of stock / listings in the market.

- Net immigration remains muted—and is likely to stay that way until the economy is more firmly on the road to recovery.

- The counterargument to this being that, with the global situation as volatile as it is, more people may opt to stick around in NZ rather than travel / move overseas.

- Jobs and economic confidence remain soft

- On the plus side, credit conditions are positive i.e. lenders are lending

The outlook on house prices

In short, the conditions just aren’t there to support a recovery in either house prices or sales volumes—so we’re likely in for another year of house prices continuing to slide sideways in nominal terms, and probably backwards in inflation-adjusted terms.

The possible exception (and one part of the housing market I’ll be watching with interest) is the $4 million+ segment.

Since Government launched its new “Golden Visa” in early March (the one requiring visa holders to build or purchase a $5m+ home) over 650 applications have been received.

Right now, there are between 3,500 – 5000 homes worth more than $5m in NZ, tightly concentrated in Auckland and Queenstown. Around 600 of those are currently listed for sale.

There will be an increase in demand in this price bracket, which could potentially see some ‘under $5m’ homes suddenly become $5m+.

Are flat house prices a bad thing?

Over the last 35 years or so, New Zealand’s economic growth has been heavily reliant on house prices tracking upwards, and that’ll be a tough habit to break.

But taking a generational view, flat house prices are arguably a good thing for people living and working in New Zealand.

Implications for investor returns

Squirrel’s Monthly Income Fund invests in loans secured by first mortgages over residential property.

The loans tend to be shorter term (less than three years) meaning the bulk of our current loan portfolio was written after house prices fell. The benefit of this is that the security for the lending is in good shape, and borrowers continue to meet their commitments.

The Squirrel Monthly Income Fund has returned 6.36%* over the last 12 months (to 31 March 2026).

Over the last interest rate cycle, the Fund returns peaked around 7.65%* p.a., giving investors a sense of the range of returns that could be expected from the Fund over time.

Based on its 8 April Monetary Policy Review, the RBNZ is expecting to deliver OCR increases starting later this year, which will flow through to retail interest rates.

The timeframe for that will be heavily dependent on how quickly the Middle East crisis and resulting oil shortages get resolved—and to what degree rising oil prices flow through to increased inflation in the economy.

That means we could see an increase to the return for investors later in the year given the loans made by the Fund have variable interest rates.

The Monthly Income Fund is a moderate risk investment aiming to deliver strong capital protection and makes monthly distributions.

So, despite ongoing weakness in the residential property market, the Fund continues to find good quality loans to invest into.

If you’re looking to keep your investments local – and hoping to ride interest rates upwards over the next few years – Squirrel’s Monthly Income Fund could be a good option to consider for the conservative to moderate risk part of your portfolio.

* Returns are net of fees and expenses and before tax.

For further information on the Squirrel Income Fund, including a copy of the Product Disclosure Statement, and to read other opinions and commentary pieces from Dave and the team at Squirrel, please visit Squirrel Landing Page on InvestNow.

Leave A Comment