India: The Missing Slice of Growth

Article written by Mugunthan Siva

Co-Founder & CIO

India Avenue

For many New Zealand investors, investing in global equities usually means exposure to Australia, the United States, Europe, and perhaps other developed markets. Yet one of the world’s notable long-term growth markets, India, is often either missing or underrepresented in portfolios. This is the first of a two-part series. Part 1 explores why India is a market worth understanding. Part 2 will look at how investors can access it.

While India’s nominal GDP ranking has recently slipped behind Japan and the United Kingdom, largely due to currency weakness and exchange rate movements rather than any deterioration in underlying economic activity, the broader outlook for the Indian economy is generally considered strong, although subject to risks and uncertainties. India is widely reported to be among the fastest growing major economies, supported by powerful structural drivers including favourable demographics, rising domestic consumption, rapid digital adoption, expanding infrastructure investment, and the ongoing development of its manufacturing and services sectors.

Short term fluctuations in currency markets may influence headline rankings measured in US dollar terms. Some forecasts suggest India could reclaim its position. With sustained growth momentum and continued structural reforms, India may have the potential to become the world’s fourth largest economy within the next few years. It could also become the third largest economy globally by the early 2030s, behind only the United States and China.

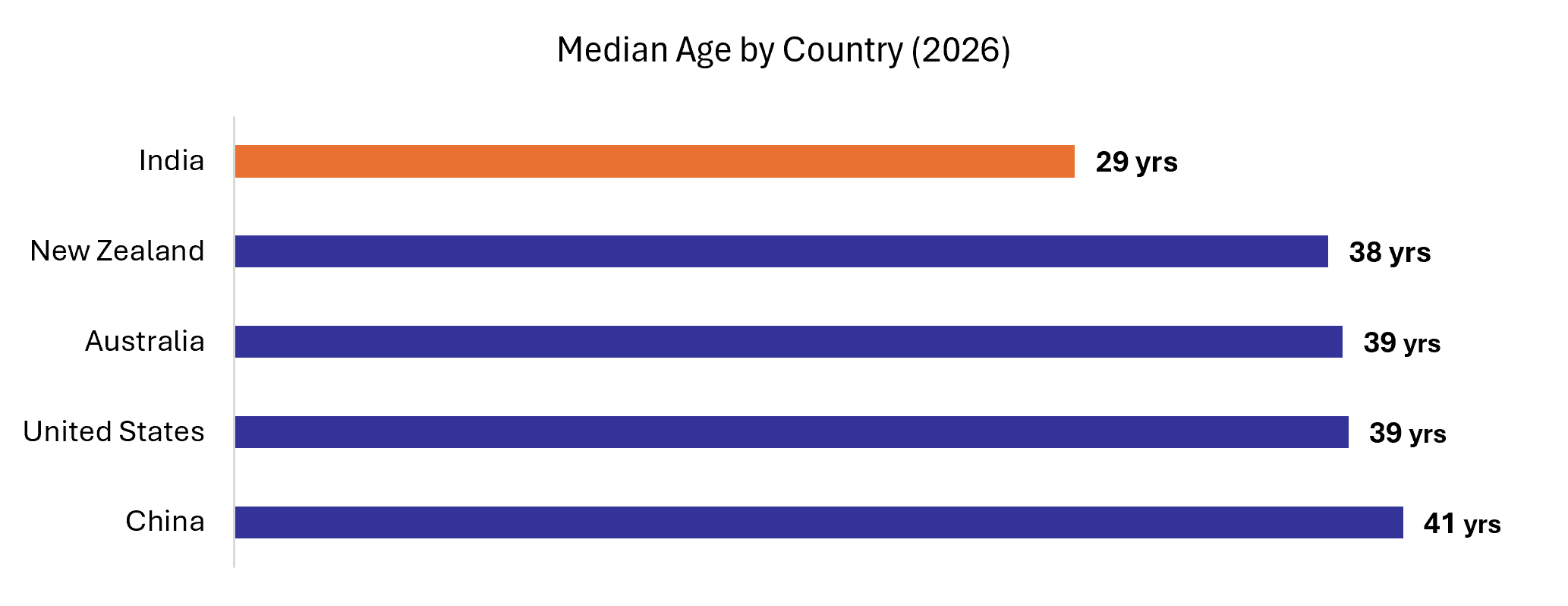

Unique Demographics

The chart below highlights one of the clearest structural differences between India and many developed economies: demographics. With a median age of just 29 years, India remains substantially younger than New Zealand, Australia, the United States, and China. This youthful population profile may provide India with a long-term economic advantage, although demographic benefits are not guaranteed and depend on policy and economic conditions, particularly as many developed economies face ageing populations, slower labour force growth, and increasing fiscal pressures associated with healthcare and retirement costs.

Figure 1: Source: Worldometer, Median Age by Country (2026)

For investors, demographics matter because economic growth is ultimately driven by people: workers, consumers, borrowers, savers, and entrepreneurs. A younger and expanding workforce can support rising productivity, stronger household formation, higher consumption, and increasing participation in financial markets over time. By contrast, ageing economies often experience slower structural growth as workforce expansion stagnates or declines.

India’s demographic advantage is further amplified by urbanisation. With only around one third of the population currently living in urban centres, India remains much earlier in its development cycle than most developed economies. The expected migration of hundreds of millions of people into cities over the coming decades may drive increased demand across housing, transport infrastructure, banking, consumer goods, healthcare, education, technology, and energy. For long term investors, these trends create exposure not just to cyclical economic growth, but to a multi decade structural transformation of the economy itself.

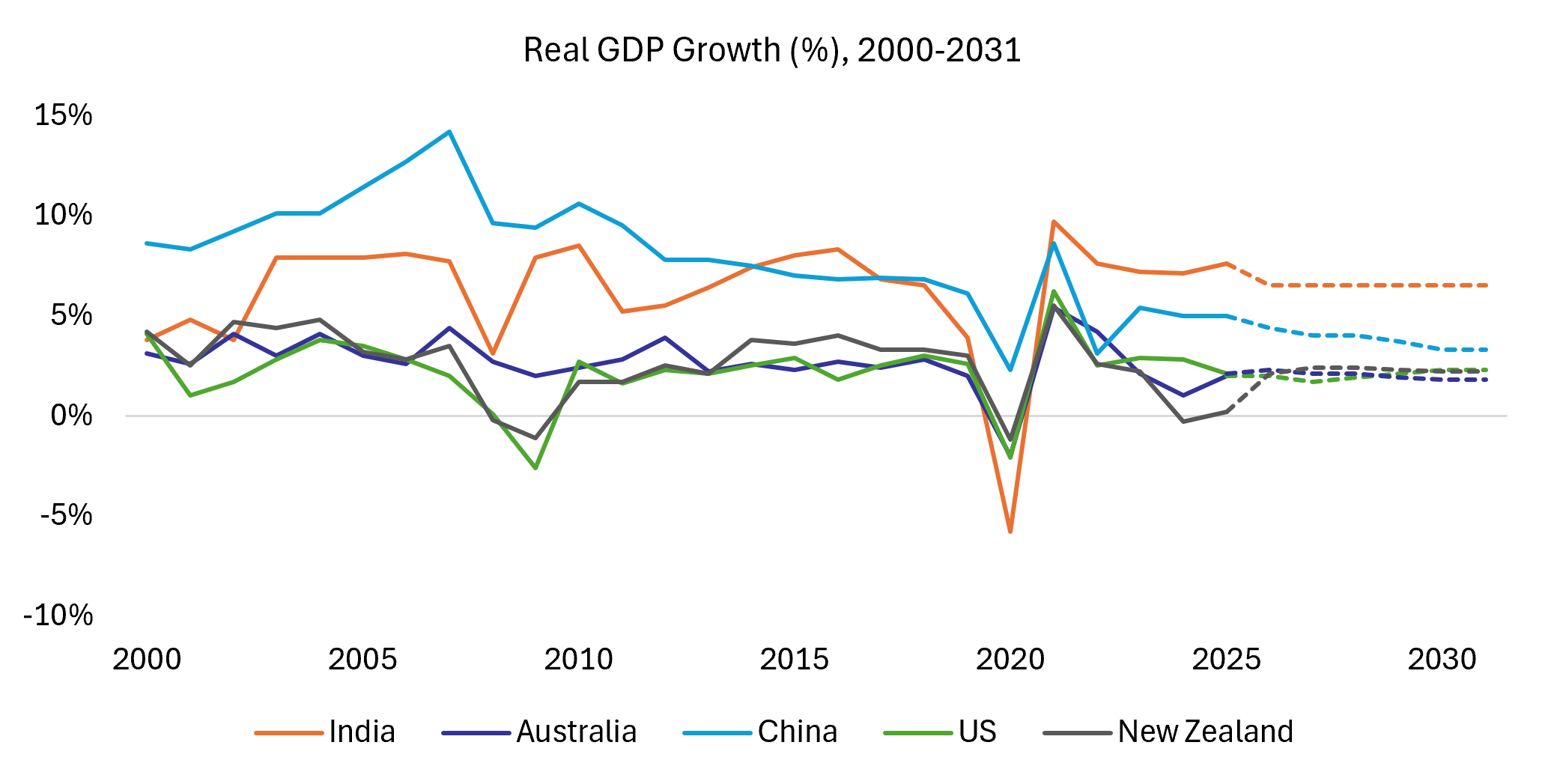

Demographics Drives GDP Growth

Figure 2: Source: International Monetary Fund, Real GDP Growth (%) 2000-2031

India’s demographic profile has been a contributing factor to its strong economic growth relative to other major economies for several consecutive years. According to the International Monetary Fund’s April 2026 World Economic Outlook, India’s real GDP growth is projected at 6.5% in 2026, comfortably ahead of China at 4.4%, the United States at 2.3%, New Zealand at 2.1%, Australia at 2.0%, and the global economy at 3.1%

What makes India’s growth story particularly compelling is that it is driven predominantly by domestic demand rather than exports. Private consumption accounts for more than 60% of GDP, which may make the economy comparatively less sensitive to certain external factors, although risks remain to global trade disruptions, geopolitical tensions, or swings in commodity prices than many export dependent emerging markets. As rising incomes support a rapidly expanding middle class, consumption led growth has been a key driver of demand across sectors including banking, technology, healthcare, consumer goods, infrastructure, transport, and financial services.

India’s progress over the past decade highlights the breadth and depth of this economic transformation. Between 2014 and 2024, India’s GDP expanded from approximately US$1.8 trillion to US$3.7 trillion, while GDP per capita increased from around US$1,560 to US$2,730.

During the same period, the number of operational airports increased from 74 to more than 200, internet users surged from 59 million to over 750 million, and annual digital transactions rose dramatically from around 1 billion to more than 100 billion. These developments reflect not only economic expansion, but also rapid improvements in connectivity, financial inclusion, digital infrastructure, and domestic productivity.

Over that period, India also rose from being the world’s 10th largest economy to one of the largest globally in nominal GDP terms, with projections continuing to point toward further gains in the years ahead. While short term currency fluctuations may affect annual rankings, the longer term structural drivers supporting India’s growth story remain firmly intact.

High GDP Growth = Robust Corporate Earnings

Strong economic growth only matters for investors if it ultimately translates into company profits. On this measure, India stands out. Over the past two decades, Indian companies delivered annualised earnings per share (EPS) growth of 9.2%, the highest among selected major equity markets. By comparison, the United States delivered 6.6%, broader emerging markets 2.7%, Australia 2.0%, and New Zealand 1.2%.

Figure 3: Source: Bloomberg, Index EPS Data (2006-2026), Data as of 30 April 2026

Just as importantly, India achieved this growth with the lowest earnings volatility among the group, at 15.1%, compared with 47.9% for Australia, 39.8% for New Zealand, 30.7% globally, and 26.9% for the United States.

This combination of strong earnings growth and relatively low volatility reflects the breadth and diversification of India’s listed market. New Zealand’s equity market is comparatively small and concentrated across a limited number of sectors. Australia’s market remains heavily influenced by banks and resource companies, making corporate earnings more sensitive to commodity prices, credit cycles, and fluctuations in global demand. Meanwhile, the United States market, although deep and highly innovative, has become increasingly concentrated in a relatively small group of large technology companies.

India offers a different type of opportunity. Its equity market provides exposure to a broad range of structural growth sectors including private sector banks, consumer businesses, healthcare, industrials, infrastructure, digital services, manufacturing, and automotive companies. Many of these industries are still at a relatively early stage of development compared with developed economies, which may indicate potential for further expansion over the long term.

Importantly, much of this growth is being driven by rising domestic participation in the economy. Millions of people are opening bank accounts for the first time, purchasing their first vehicle, taking out insurance policies, accessing healthcare services, investing digitally, or connecting to the internet. As incomes rise and urbanisation accelerates, these trends support sustained demand across large parts of the economy, which may support ongoing earnings growth, although this is not guaranteed.

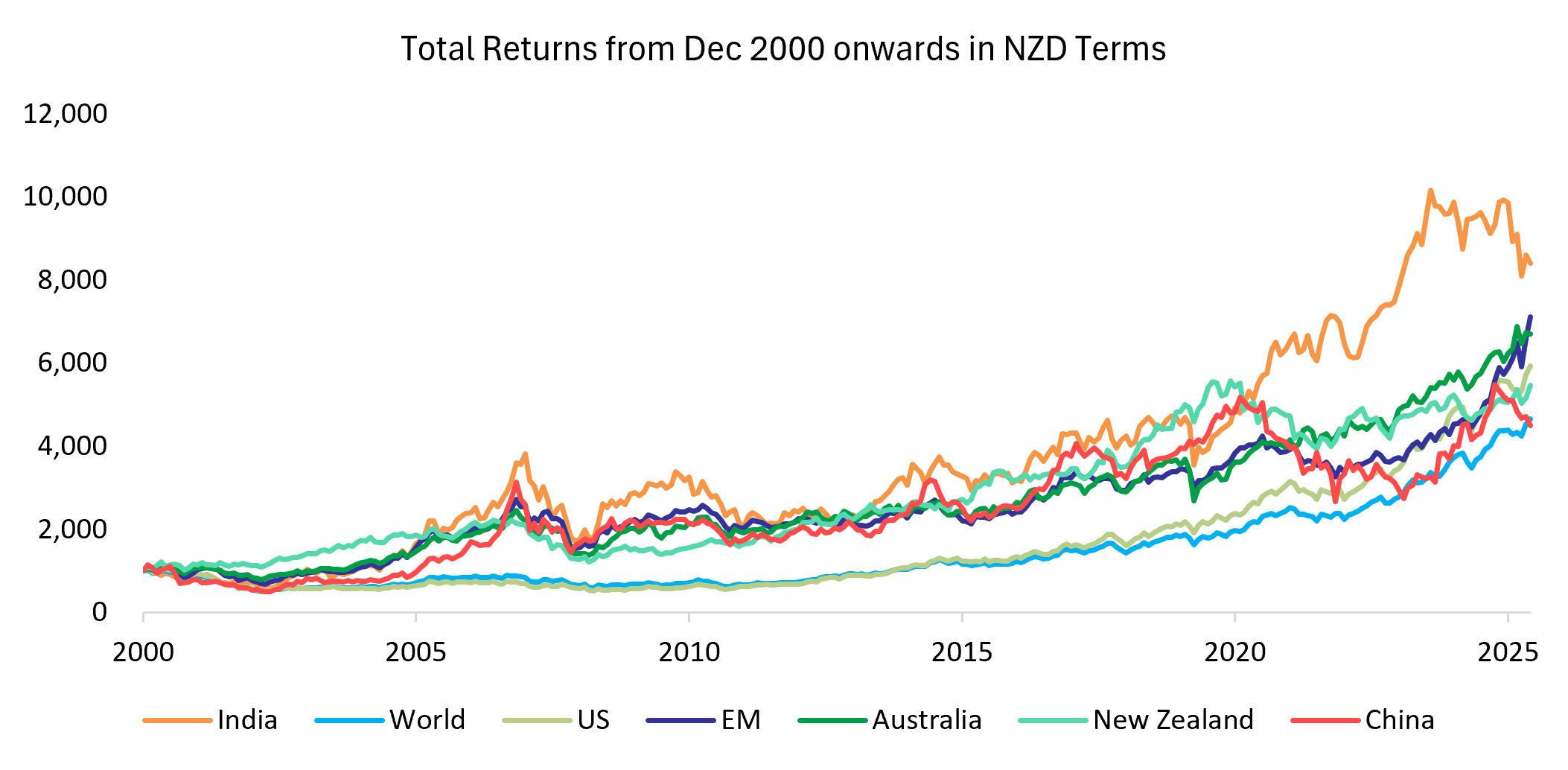

Returns from India Equity Markets

Figure 4: Source: MSCI, Data as of 30 April 2026

Historically, returns from Indian equities have outperformed many major equity markets over the past two decades, including global equities, broader emerging markets, Australian equities, and New Zealand equities. When viewed in New Zealand dollar terms, the extent of this historical outperformance becomes even more apparent.

This performance reflects the powerful combination of structural drivers underpinning the Indian economy: favourable demographics, a rapidly expanding working age population, rising urbanisation, increasing household incomes, and sustained domestic consumption. These factors have supported relatively strong GDP growth (compared to many economies), creating an environment in which businesses have been able to grow revenues, expand earnings, and reinvest capital over long periods of time.

Importantly, India’s equity market performance has not simply been driven by short term market sentiment or speculative growth. Rather, it has been supported by broad based corporate earnings expansion across sectors such as private banking, consumer goods, healthcare, infrastructure, technology, financial services, manufacturing, and industrials. As millions of people continue to enter the formal economy, access financial services, purchase consumer products, and participate in digital and urban economic activity for the first time, may provide Indian companies with ongoing domestic growth opportunities.

For investors seeking long term growth exposure within diversified portfolios, India may offer a differentiated exposure within a diversified portfolio. While many developed markets face slower population growth, ageing demographics, and more mature economic structures, India remains earlier in its development cycle with significant room for expansion across consumption, infrastructure, productivity, and financial penetration. This combination of structural economic growth and strong corporate earnings growth has been one factor associated with India’s historical long-term equity market returns and may continue to be relevant within global investment portfolios for many years ahead, although future outcomes are uncertain.

Looking Ahead

India is not without risk. Investors should expect periods of market volatility, changing valuations, currency fluctuations, and shifts in government policy or global trade conditions. Like all emerging markets, returns are unlikely to move in a straight line, and sentiment toward India can change quickly during periods of global uncertainty.

However, an important consideration for investors is: Can global portfolios afford to overlook one of the world’s largest and fastest growing economies?

India combines several characteristics that may be less common among some other markets; a young and growing population, strong structural economic growth, rising corporate profitability, increasing urbanisation, expanding digital and financial inclusion, and a broad, diversified equity market. Importantly, many of these growth drivers remain at a relatively early stage compared with developed economies, suggesting that the opportunity set could extend over a long period, although this is not assured.

For New Zealand investors in particular, India may provide exposure to a different source of returns. Most domestic portfolios remain heavily exposed to developed markets such as New Zealand, Australia, and the United States; economies that are generally more mature, slower growing, and increasingly affected by ageing demographics. India may provide exposure to a different part of the global growth cycle, driven primarily by domestic consumption, infrastructure development, and rising middle class participation.

India’s importance within the global economy continues to expand. Yet its representation within many investor portfolios remains comparatively small. That gap may indicate a potential area of interest for investors available in global equities today.

If you’d like to learn more about the India Avenue Equity Fund, please refer to the Product Disclosure Statement and other disclosure material available on India Avenue landing page on InvestNow.

Disclaimer:

- A copy of the PDS for the India Avenue Equity Fund (H Class) can be obtained by writing to India Avenue on IA@indianavenue.com.au or by visiting www.indiaavenue.com.au.

- Equity Trustees Limited is the Responsible Entity (ABN 46 004 031 298, AFSL 240975) for the India Avenue Equity Fund (H Class).

- This Note (‘Note’) has been produced by India Avenue Investment Management Limited (‘IAIM’) ABN 38 604 095 954, AFSL 478233 and has been prepared for informational and discussion purposes only. This does not constitute an offer to sell or a solicitation of an offer to purchase any security or financial product or service. Any such offer or solicitation shall be made only pursuant to a Product Disclosure Statement, Information Memorandum, or other offer document (collectively ‘Offer Document’) relating to an IAIM financial product or service.

- This Note does not constitute a part of any Offer Document issued by IAIM. The information contained in this Note may not be reproduced, used, or disclosed, in whole or in part, without prior written consent of IAIM.

- Past performance is not necessarily indicative of future results and no person guarantees the performance of any IAIM financial product or service or the amount or timing of any return from it. There can be no assurance that an IAIM financial product or service will achieve any targeted returns, that asset allocations will be met or that an IAIM financial product or service will be able to implement its investment strategy and investment approach or achieve its investment objective.

- Statements contained in this Note that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of IAIM. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Additionally, this Note may contain “forward-looking statements”. Actual events or results or the actual performance of an IAIM financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. Nothing contained herein should be construed as granting by implication, or otherwise, any license or right to use any trademark displayed without the written permission of the owner.

- Certain economic, market or company information contained herein has been obtained from published sources prepared by third parties. While such sources are believed to be reliable, neither IAIM nor any of its respective officers or employees assumes any responsibility for the accuracy or completeness of such information. None of IAIM or any of its respective officers or employees has made any representation or warranty, express or implied, with respect to the correctness, accuracy, reasonableness or completeness of any of the information contained in this and they expressly disclaim any responsibility or liability, therefore. No person, including IAIM has any responsibility to update any of the information provided in this Note.

- Neither this Note nor the provision of any Offer Document issued by IAIM is, and must not be regarded as, advice or a recommendation or opinion in relation to an IAIM financial product or service, or that an investment in an IAIM financial product or service is suitable for you or any other person. Neither this Note nor any Offer Document issued by IAIM considers your investment objectives, financial situation, and particular needs. In addition to carefully reading the relevant Offer Document issued by IAIM you should, before deciding whether to invest in an IAIM financial product or service, consider the appropriateness of investing or continuing to invest, having regard to your own objectives, financial situation, or needs. IAIM strongly recommends that you obtain independent financial, legal and taxation advice before deciding whether to invest in an IAIM financial product or service.

This information is provided by InvestNow Saving and Investment Service Limited (“InvestNow”). The information and any opinions in this publication are based on sources that InvestNow believes are reliable and accurate. InvestNow, its directors, officers and employees make no representations or warranties of any kind as to the accuracy or completeness of the information contained in this publication and disclaim liability for any loss, damage, cost or expense that may arise from any reliance on the information or any opinions, conclusions or recommendations contained in it, whether that loss or damage is caused by any fault or negligence on the part of InvestNow, or otherwise, except for any statutory liability which cannot be excluded. All opinions and market commentary reflect InvestNow’s judgment on the date of this publication and are subject to change without notice. This disclaimer extends to any entity that may distribute this publication. The information in this publication is not intended to be financial advice for the purposes of the Financial Markets Conduct Act 2013, as amended by the Financial Services Legislation Amendment Act 2019. In particular, in preparing this document, InvestNow did not take into account the investment objectives, financial situation and particular needs of any particular person. Professional investment advice from an appropriately qualified adviser is recommended before making any investment. All Investments involve risk. Examples of specific fund performance are for illustrative purposes only and are not intended as a recommendation. Any projections, scenarios, or modelling presented are illustrative only and are not forecasts or predictions of future performance. Past performance is not a reliable indicator of future results.

Leave A Comment