Volatility, rotation and keeping perspective

Pie Funds’ founder and Chief Investment Officer Mike Taylor explains why February’s market rotation is a reminder that sentiment can shift quickly – but fundamentals rarely move as fast as prices.

A complicated start to March

By the time you’re reading this it’s mid-late March and the world looks even more complicated than it did at the end of February.

A war has erupted in the Middle East. Oil prices have swung sharply as markets try to assess whether the conflict spreads or remains contained. Central banks are still wrestling with inflation. And investors are again asking the perennial question: what does this mean for markets?

Geopolitical events always introduce uncertainty. Markets don’t like uncertainty and conflicts tend to amplify volatility across asset classes – equities, bonds, currencies and commodities.

So before anything else, yes, we are watching events very closely. We are stress testing portfolios. We are adjusting position sizes where required. And we are constantly reviewing price-to-fair-value assumptions as new information emerges.

That’s our job.

It’s important to say though that the conflict does not change February’s results. February was actually a constructive month for markets overall despite the volatility and despite the sharp sector rotations that dominated headlines.

What we saw was less about a collapse in fundamentals and more about the market reacting quickly to a shift in narrative.

The AI narrative that moved markets

As I mentioned on LinkedIn recently, an online piece from Citrini Research triggered a meaningful shift in positioning and investor thinking.

The thesis was bold: that artificial intelligence (“AI”) could drive US unemployment from around 4% today to potentially 10% within two years.

Whether you agree with that view or not, markets responded immediately.

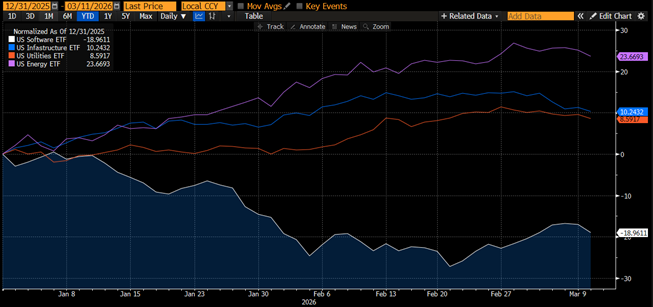

As shown in the chart below, technology and software stocks (white line) sold off aggressively as investors tried to price in the possibility that AI could disrupt parts of the digital economy sooner than expected. Capital rotated rapidly into what investors perceived as “hard assets” or more defensive exposures.

That meant flows into areas such as infrastructure, energy, materials and parts of the industrial economy (blue, red, purple lines).

Capital rotating away from tech and software: January-March 2026

Source: Bloomberg

When positioning changes that quickly, prices move quickly too.

And that’s exactly what we saw in February.

The interesting thing is that these moves were driven far more by narrative than by any meaningful change in underlying earnings or economic data.

When markets overreact to narratives

It’s also worth remembering that even leaders within the AI ecosystem pushed back on the idea that artificial intelligence is hollowing out the labour market.

Anthropic executives questioned the unemployment thesis. Nvidia’s Jensen Huang pointed out that AI adoption historically tends to create new categories of work rather than eliminate them entirely.

And interestingly, job postings for software engineers have actually begun rising again after a soft period last year.

Markets can overreact to narratives, especially when positioning is stretched.

When a new idea captures investor attention, capital tends to move quickly and often overshoots.

That doesn’t mean the narrative is wrong. AI will absolutely reshape industries. But the pace of change is rarely as immediate as markets sometimes assume.

In the meantime, fundamentals continue to evolve at a much slower and more predictable pace.

Oil volatility and geopolitical risk

The other story developing as we moved into March has been the volatility in oil markets.

Energy markets are always highly sensitive to geopolitical developments, particularly in the Middle East given the region’s importance to global supply.

As the chart below shows, oil prices have moved sharply upwards as traders try to assess whether the conflict affects shipping routes, production capacity or broader regional stability.

Brent crude oil price: Sept 2025 – 9 March 2026

Source: Bloomberg

Oil volatility matters because it feeds into inflation expectations. If energy prices spike meaningfully, central banks may be forced to keep interest rates higher for longer.

At the moment the situation remains fluid. Markets are trying to determine whether this becomes a prolonged supply disruption or simply another geopolitical shock that eventually fades.

History suggests most geopolitical oil spikes prove temporary unless supply is materially disrupted.

But in the short term, the uncertainty adds another layer of complexity for investors already navigating interest-rate and technology-driven market shifts.

Volatility is the price of admission

At Pie we’ve now lived through the Global Financial Crisis, the European debt crisis, Covid, inflation shocks, the Ukraine war, banking stress events and countless geopolitical flare-ups since 2007.

Every one of them felt uncomfortable in the moment.

None of them justified abandoning disciplined long-term investing.

Volatility is not new. It’s simply the price of admission for participating in markets.

And, more often than not, volatility creates opportunity.

When markets move quickly and sentiment overshoots, long-term investors get the chance to buy quality businesses or assets at better prices.

That’s why periods of uncertainty tend to reward investors who remain disciplined and focused on fundamentals rather than short-term narratives.

Looking ahead: the next quarter

Looking forward to the next quarter, there are three themes we’re watching closely.

First, interest rates.

Central banks remain the biggest driver of market sentiment, with the US 10-year bond yield chart below showing this at play. Inflation has eased but not disappeared, and policymakers are trying to balance economic growth with price stability. Markets will continue to react quickly to changes in interest-rate expectations.

US 10-year bond yield trend: last 12 months

Source: Bloomberg

Second, the breadth of the equity rally.

For much of the past year a small group of mega-cap technology stocks dominated global market returns. More recently we’ve started to see performance broaden across sectors and regions. That’s generally a healthier backdrop for markets, and one of the reasons why indices like the S&P 500 continue to move higher, as the chart below shows.

Market breadth is increasing: S&P 500 past 5 years

Source: Bloomberg

Third, the evolution of the AI investment cycle.

Artificial intelligence will remain one of the defining economic themes of the next decade. But markets will continue to cycle between optimism and scepticism as investors debate how quickly those investments translate into real economic value.

These debates will drive short-term volatility, but the long-term direction of travel remains clear.

Keeping perspective

If there’s one lesson markets teach repeatedly, it’s that sentiment moves faster than fundamentals.

Narratives come and go. Headlines change daily.

But businesses, earnings and economic trends evolve far more gradually.

Our job as investors is not to react emotionally to every narrative shift. It is to stay focused on underlying value, assess risk carefully and take advantage of opportunities when markets misprice assets.

Interesting times? Absolutely.

But we remain calm, engaged and doing the work – just like we always have.

If you want to see which Pie Funds investments are available on InvestNow, plus read any other opinion or commentary pieces from Mike and the team at Pie Funds, please visit their page on our website.

Volatility, rotation and keeping perspective

Pie Funds’ founder and Chief Investment Officer Mike Taylor explains why February’s market rotation is a reminder that sentiment can shift quickly – but fundamentals rarely move as fast as prices.

A complicated start to March

By the time you’re reading this it’s mid-late March and the world looks even more complicated than it did at the end of February.

A war has erupted in the Middle East. Oil prices have swung sharply as markets try to assess whether the conflict spreads or remains contained. Central banks are still wrestling with inflation. And investors are again asking the perennial question: what does this mean for markets?

Geopolitical events always introduce uncertainty. Markets don’t like uncertainty and conflicts tend to amplify volatility across asset classes – equities, bonds, currencies and commodities.

So before anything else, yes, we are watching events very closely. We are stress testing portfolios. We are adjusting position sizes where required. And we are constantly reviewing price-to-fair-value assumptions as new information emerges.

That’s our job.

It’s important to say though that the conflict does not change February’s results. February was actually a constructive month for markets overall despite the volatility and despite the sharp sector rotations that dominated headlines.

What we saw was less about a collapse in fundamentals and more about the market reacting quickly to a shift in narrative.

The AI narrative that moved markets

As I mentioned on LinkedIn recently, an online piece from Citrini Research triggered a meaningful shift in positioning and investor thinking.

The thesis was bold: that artificial intelligence (“AI”) could drive US unemployment from around 4% today to potentially 10% within two years.

Whether you agree with that view or not, markets responded immediately.

As shown in the chart below, technology and software stocks (white line) sold off aggressively as investors tried to price in the possibility that AI could disrupt parts of the digital economy sooner than expected. Capital rotated rapidly into what investors perceived as “hard assets” or more defensive exposures.

That meant flows into areas such as infrastructure, energy, materials and parts of the industrial economy (blue, red, purple lines).

Capital rotating away from tech and software: January-March 2026

Source: Bloomberg

When positioning changes that quickly, prices move quickly too.

And that’s exactly what we saw in February.

The interesting thing is that these moves were driven far more by narrative than by any meaningful change in underlying earnings or economic data.

When markets overreact to narratives

It’s also worth remembering that even leaders within the AI ecosystem pushed back on the idea that artificial intelligence is hollowing out the labour market.

Anthropic executives questioned the unemployment thesis. Nvidia’s Jensen Huang pointed out that AI adoption historically tends to create new categories of work rather than eliminate them entirely.

And interestingly, job postings for software engineers have actually begun rising again after a soft period last year.

Markets can overreact to narratives, especially when positioning is stretched.

When a new idea captures investor attention, capital tends to move quickly and often overshoots.

That doesn’t mean the narrative is wrong. AI will absolutely reshape industries. But the pace of change is rarely as immediate as markets sometimes assume.

In the meantime, fundamentals continue to evolve at a much slower and more predictable pace.

Oil volatility and geopolitical risk

The other story developing as we moved into March has been the volatility in oil markets.

Energy markets are always highly sensitive to geopolitical developments, particularly in the Middle East given the region’s importance to global supply.

As the chart below shows, oil prices have moved sharply upwards as traders try to assess whether the conflict affects shipping routes, production capacity or broader regional stability.

Brent crude oil price: Sept 2025 – 9 March 2026

Source: Bloomberg

Oil volatility matters because it feeds into inflation expectations. If energy prices spike meaningfully, central banks may be forced to keep interest rates higher for longer.

At the moment the situation remains fluid. Markets are trying to determine whether this becomes a prolonged supply disruption or simply another geopolitical shock that eventually fades.

History suggests most geopolitical oil spikes prove temporary unless supply is materially disrupted.

But in the short term, the uncertainty adds another layer of complexity for investors already navigating interest-rate and technology-driven market shifts.

Volatility is the price of admission

At Pie we’ve now lived through the Global Financial Crisis, the European debt crisis, Covid, inflation shocks, the Ukraine war, banking stress events and countless geopolitical flare-ups since 2007.

Every one of them felt uncomfortable in the moment.

None of them justified abandoning disciplined long-term investing.

Volatility is not new. It’s simply the price of admission for participating in markets.

And, more often than not, volatility creates opportunity.

When markets move quickly and sentiment overshoots, long-term investors get the chance to buy quality businesses or assets at better prices.

That’s why periods of uncertainty tend to reward investors who remain disciplined and focused on fundamentals rather than short-term narratives.

Looking ahead: the next quarter

Looking forward to the next quarter, there are three themes we’re watching closely.

First, interest rates.

Central banks remain the biggest driver of market sentiment, with the US 10-year bond yield chart below showing this at play. Inflation has eased but not disappeared, and policymakers are trying to balance economic growth with price stability. Markets will continue to react quickly to changes in interest-rate expectations.

US 10-year bond yield trend: last 12 months

Source: Bloomberg

Second, the breadth of the equity rally.

For much of the past year a small group of mega-cap technology stocks dominated global market returns. More recently we’ve started to see performance broaden across sectors and regions. That’s generally a healthier backdrop for markets, and one of the reasons why indices like the S&P 500 continue to move higher, as the chart below shows.

Market breadth is increasing: S&P 500 past 5 years

Source: Bloomberg

Third, the evolution of the AI investment cycle.

Artificial intelligence will remain one of the defining economic themes of the next decade. But markets will continue to cycle between optimism and scepticism as investors debate how quickly those investments translate into real economic value.

These debates will drive short-term volatility, but the long-term direction of travel remains clear.

Keeping perspective

If there’s one lesson markets teach repeatedly, it’s that sentiment moves faster than fundamentals.

Narratives come and go. Headlines change daily.

But businesses, earnings and economic trends evolve far more gradually.

Our job as investors is not to react emotionally to every narrative shift. It is to stay focused on underlying value, assess risk carefully and take advantage of opportunities when markets misprice assets.

Interesting times? Absolutely.

But we remain calm, engaged and doing the work – just like we always have.

If you want to see which Pie Funds investments are available on InvestNow, plus read any other opinion or commentary pieces from Mike and the team at Pie Funds, please visit their page on our website.

Leave A Comment