")

Why markets keep rising despite global uncertainty

Amova Asset Management’s Portfolio Manager, Alan Clarke, shares his take on April’s strong market rebound and the key forces driving returns. From geopolitical tensions to the ongoing rise of AI, he explains why short-term market swings can distract from what really matters – long-term earnings growth.

Market Recap

As at the close of April global equities were up just over 6% in local currency terms for the first 4 months of 2026. Nothing remarkable in that, and one might assume it had merely been a continuation of the strong returns from global share markets dating back to late 2022. But the April 2026 return (up over 9% in local currency terms) joined a short-list of near-record high monthly returns. Over the last 30 years, the only months that delivered larger gains were April and November 2020 in the Covid period, and April 2009 when markets rebounded from the depths of the global financial crisis. Markets recovered sharply from the brief sell-down in the prior month triggered by the outbreak of war in the Middle East. While the conflict in the Middle East is far from over, markets took comfort from a partial truce and movements towards a longer-term agreement. Oil prices remained elevated with Brent Crude trading at U$114 per barrel at month end, down from the highs reached in March, but still well above the U$60-90 range they have traded in for most of the last few years.

Returns from bonds over April were more muted, global bonds and NZ bond markets were up 0.2% and 0.3% respectively, and both are slightly negative year to date. Higher energy prices and the impact they may have on economic growth and inflation has impacted bond yields at the short and long end of the curve. Central bankers have become slightly less dovish, and in some case like Australia more hawkish, acknowledging the risk high energy prices could have on inflation expectations.

The Voting Machine and The Weighing Machine

Given the remarkable macro events that have unfolded recently, and indeed those over the last six-plus years going back to the outbreak of Covid, it does seem slightly counter-intuitive to be talking about stock markets trading at or near all-time highs. So, what else helps explain the remarkable returns seen not just over April, but over the last 3+ years? A large part of the answer is earnings power, that is the level and growth of earnings. Legendary investor Benjamin Graham, who literally wrote the book on investing (well, one of the first books) said “in the short run, the share market is a voting machine, but in the long run, it is a weighing machine”. The ‘votes’ are driven by the ever-increasing short-term noise; geo-political conflict, elections, central bank movements, economic data announcements, quarterly earnings beats and misses. John Maynard Keynes, another Hall-of-Famer in terms of investing and book-writing, referred to this as ‘animal spirits’ in describing the instinctive and emotional factors that influence human behavior, and therefore overall market sentiment. The ‘weighing machine’ on the other hand, is measuring the earnings power that should dictate long-term returns that investors will benefit from.

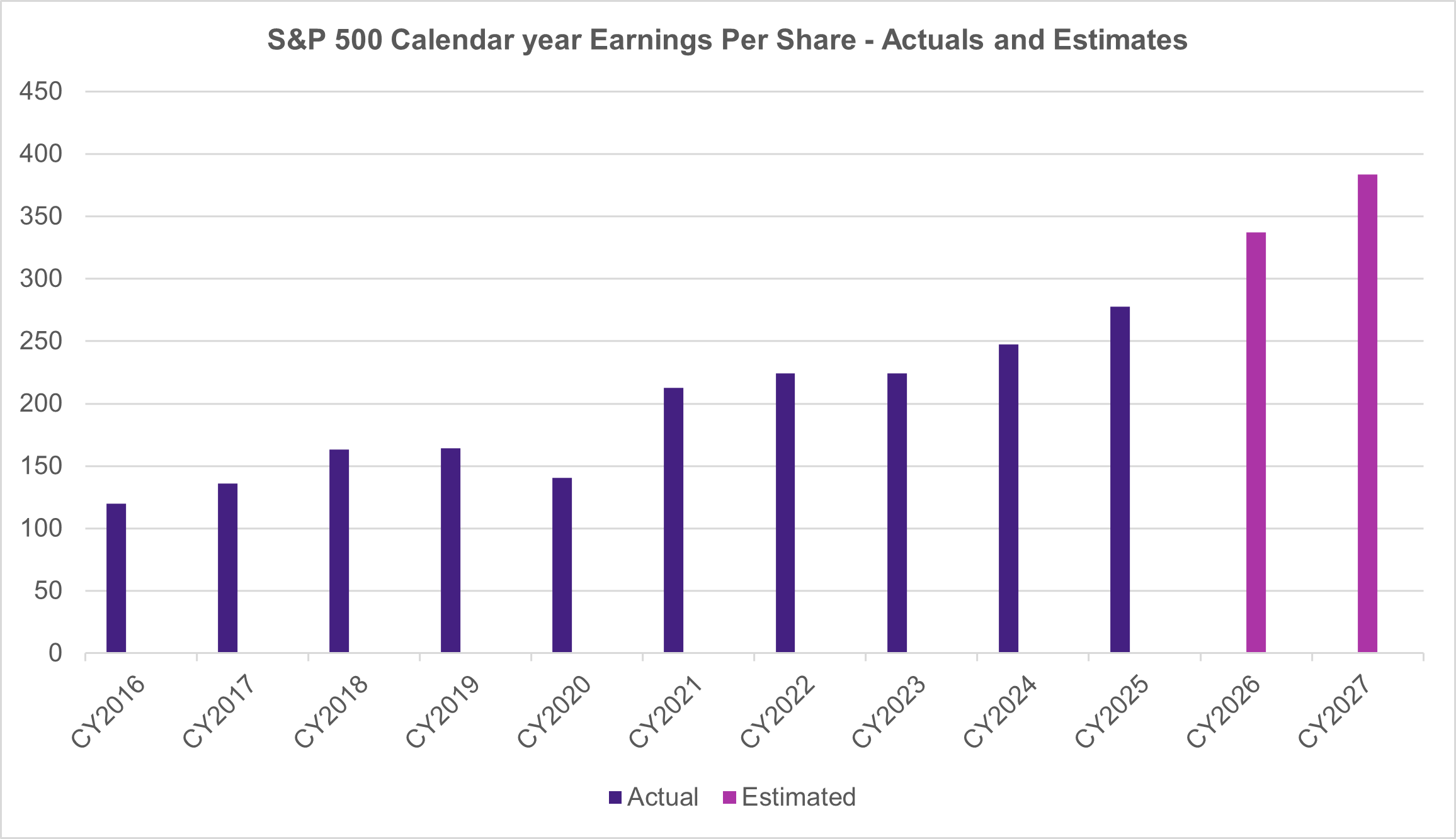

Figure 1 below shows the growth of one-year earnings for the S&P500 over the last 10 years. The US is one of the few countries where the share-market does reflect the overall economy. It comprises companies across nearly all sectors/industries, and is at least partially exposed to whatever new innovations, technologies, products, services are being developed, as well as plenty of ‘old economy’ businesses that make up the less exciting part of the economy. So, a large part of the earnings growth shown below will be from ‘big-Tech’ from the late 2010’s, and more recently from the evolution and roll-out of AI. US equities have outperformed nearly all other regions over the last 10 years, but this has been supported by the earnings power delivered by the aggregation of companies that make up the US equity market.

Figure 1: S&P 500 Calendar Year Bottom-Up Earnings Per Share – Actuals and Estimates

Source: Bloomberg, Amova Asset Management

The AI juggernaut rolls on

While the more positive developments in the Middle East conflict certainly contributed to improved market sentiment in April, the continued development and roll-out of all things AI also contributed. Earnings season saw a number of companies report strong profit growth, and more importantly forward guidance on planned capital expenditure within the evolving AI ecosystem was ratcheted up yet again. Because one company’s CapEx is another company’s revenue, the beneficiaries of this spend saw continued strong earnings performance and optimistic earnings outlook. The best performing industry group for the month was semi-conductors, up over 27% for the month, and now up nearly 120% over the 12-month period! This strength was reflected in terms of country returns where South Korea (+31%) and Taiwan (+23%) outperformed due to their national champions – Samsung and SK Hynik in Korea and TSMC in Tawain – making up an ever-increasing component of both domestic share markets.

Another positive aspect of the recent earning season has been the breadth in earnings outside of the Technology and Energy sectors. Earnings outlooks at the start of the year are usually overly optimistic and get gradually lowered as the year progresses. Given the macro-economic environment, it would have been no surprise if this year had followed a similar pattern. So far this hasn’t been the case, and aggregate revenue expectations, profit margins and forecast net profits have held up well.

So what should investors focus on in this mad, mad world?

The March/April period was the second time in just over a year that global share markets have whip-sawed down and then up on the back of geo-politics. In April 2025 markets fell over 10% in a matter of days after the US administration ‘Liberation Day’ announcement of a new world order for global trade. They then rebounded just as quickly when the initial tariff levels were watered down. Following the late February outbreak of the hostilities in Iran, global shares were down over 8% towards the end of March. Remarkedly by mid-April they bounced back to be making new record highs. While these movements are invariably uncomfortable for investors, they will almost certainly continue to feature in an ever-changing world where news -and therefore noise – is circulated and consumed at ever increasing speeds. Investors should use these periods as a reminder to focus on their longer-term savings goals and not join in too much on the exercise of ‘voting’ on where share markets go in the short term.

If you’d like to learn more about the Amova Asset Management funds on InvestNow, please visit the Amova landing page on InvestNow.

")

Why markets keep rising despite global uncertainty

Amova Asset Management’s Portfolio Manager, Alan Clarke, shares his take on April’s strong market rebound and the key forces driving returns. From geopolitical tensions to the ongoing rise of AI, he explains why short-term market swings can distract from what really matters – long-term earnings growth.

Market Recap

As at the close of April global equites were up just over 6% in local currency terms for the first 4 months of 2026. Nothing remarkable in that, and one might assume it had merely been a continuation of the strong returns from global share markets dating back to late 2022. But the April 2026 return (up over 9% in local currency terms) joined a short-list of near-record high monthly returns. Over the last 30 years, the only months that delivered larger gains were April and November 2020 in the Covid period, and April 2009 when markets rebounded from the depths of the global financial crisis. Markets recovered sharply from the brief sell-down in the prior month triggered by the outbreak of war in the Middle East. While the conflict in the Middle East is far from over, markets took comfort from a partial truce and movements towards a longer-term agreement. Oil prices remained elevated with Brent Crude trading at U$114 per barrel at month end, down from the highs reached in March, but still well above the U$60-90 range they have traded in for most of the last few years.

Returns from bonds over April were more muted, global bonds and NZ bond markets were up 0.2% and 0.3% respectively, and both are slightly negative year to date. Higher energy prices and the impact they may have on economic growth and inflation has impacted bond yields at the short and long end of the curve. Central bankers have become slightly less dovish, and in some case like Australia more hawkish, acknowledging the risk high energy prices could have on inflation expectations.

The Voting Machine and The Weighing Machine

Given the remarkable macro events that have unfolded recently, and indeed those over the last six-plus years going back to the outbreak of Covid, it does seem slightly counter-intuitive to be talking about stock markets trading at or near all-time highs. So, what else helps explain the remarkable returns seen not just over April, but over the last 3+ years? A large part of the answer is earnings power, that is the level and growth of earnings. Legendary investor Benjamin Graham, who literally wrote the book on investing (well, one of the first books) said “in the short run, the share market is a voting machine, but in the long run, it is a weighing machine”. The ‘votes’ are driven by the ever-increasing short-term noise; geo-political conflict, elections, central bank movements, economic data announcements, quarterly earnings beats and misses. John Maynard Keynes, another Hall-of-Famer in terms of investing and book-writing, referred to this as ‘animal spirits’ in describing the instinctive and emotional factors that influence human behavior, and therefore overall market sentiment. The ‘weighing machine’ on the other hand, is measuring the earnings power that should dictate long-term returns that investors will benefit from.

Figure 1 below shows the growth of one-year earnings for the S&P500 over the last 10 years. The US is one of the few countries where the share-market does reflect the overall economy. It comprises companies across nearly all sectors/industries, and is at least partially exposed to whatever new innovations, technologies, products, services are being developed, as well as plenty of ‘old economy’ businesses that make up the less exciting part of the economy. So, a large part of the earnings growth shown below will be from ‘big-Tech’ from the late 2010’s, and more recently from the evolution and roll-out of AI. US equities have outperformed nearly all other regions over the last 10 years, but this has been supported by the earnings power delivered by the aggregation of companies that make up the US equity market.

Figure 1: S&P 500 Calendar Year Bottom-Up Earnings Per Share – Actuals and Estimates

Source: Bloomberg, Amova Asset Management

The AI juggernaut rolls on

While the more positive developments in the Middle East conflict certainly contributed to improved market sentiment in April, the continued development and roll-out of all things AI also contributed. Earnings season saw a number of companies report strong profit growth, and more importantly forward guidance on planned capital expenditure within the evolving AI ecosystem was ratcheted up yet again. Because one company’s CapEx is another company’s revenue, the beneficiaries of this spend saw continued strong earnings performance and optimistic earnings outlook. The best performing industry group for the month was semi-conductors, up over 27% for the month, and now up nearly 120% over the 12-month period! This strength was reflected in terms of country returns where South Korea (+31%) and Taiwan (+23%) outperformed due to their national champions – Samsung and SK Hynik in Korea and TSMC in Tawain – making up an ever-increasing component of both domestic share markets.

Another positive aspect of the recent earning season has been the breadth in earnings outside of the Technology and Energy sectors. Earnings outlooks at the start of the year are usually overly optimistic and get gradually lowered as the year progresses. Given the macro-economic environment, it would have been no surprise if this year had followed a similar pattern. So far this hasn’t been the case, and aggregate revenue expectations, profit margins and forecast net profits have held up well.

So what should investors focus on in this mad, mad world?

The March/April period was the second time in just over a year that global share markets have whip-sawed down and then up on the back of geo-politics. In April 2025 markets fell over 10% in a matter of days after the US administration ‘Liberation Day’ announcement of a new world order for global trade. They then rebounded just as quickly when the initial tariff levels were watered down. Following the late February outbreak of the hostilities in Iran, global shares were down over 8% towards the end of March. Remarkedly by mid-April they bounced back to be making new record highs. While these movements are invariably uncomfortable for investors, they will almost certainly continue to feature in an ever-changing world where news -and therefore noise – is circulated and consumed at ever increasing speeds. Investors should use these periods as a reminder to focus on their longer-term savings goals and not join in too much on the exercise of ‘voting’ on where share markets go in the short term.

If you’d like to learn more about the Amova Asset Management funds on InvestNow, please visit the Amova landing page on InvestNow.

Leave A Comment