")

Signs of Calm as Markets Recover Momentum

Global markets appeared to regain momentum in May, supported by strong earnings and easing geopolitical tensions. While risks remain, the backdrop improved for investors. Del Hart shares what drove markets, what it means, and the key themes to watch next.

Introduction

May 2026 saw global markets resume a risk-on tone after a turbulent period of trade policy and geopolitical uncertainty. Strong corporate earnings – particularly from technology firms exposed to AI demand – together with signs of de‑escalation in some geopolitical flashpoints, supported equity markets. At the same time, energy-market developments and a leadership transition at the US Federal Reserve added fresh sources of volatility and policy uncertainty. Against that backdrop, bond yields moved unevenly, commodity prices fell from April peaks, and the New Zealand economy showed mixed domestic momentum amid sticky inflation.

Economic overview

US trade policy continued to shape market narratives. A series of targeted tariffs introduced earlier in 2025 and 2026 remained in place for several product categories, and ongoing bilateral negotiations produced episodic headlines. Markets reacted more to earnings momentum and geopolitics in May than to fresh tariff shocks, but the lingering tariff regime continues to represent a structural headwind for global trade and supply chains.

The US macro picture remained resilient in aggregate. May was dominated by solid corporate earnings – led by semiconductor and software firms capitalising on AI demand – which helped lift investor sentiment. However, business surveys and some cyclical indicators signalled slowing manufacturing momentum. Inflation dynamics showed regional divergence: services inflation remained persistent in parts of the US, while goods inflation eased as energy prices moderated late in the month.

In China, policymakers maintained an accommodative stance to support growth, while European economies continued to battle soft demand even as fiscal measures in some countries provided a partial offset. Global growth forecasts were nudged modestly higher on resilient activity data, although downside risks from a renewed Middle East energy shock remained present.

New Zealand’s Q1 2026 inflation print confirmed higher-than-expected price pressures, with annual CPI around the low 3% area and notable contributions from housing‑related costs and utilities. Against that backdrop, the RBNZ kept the Official Cash Rate on hold at its May meeting, citing both persistent domestic inflation pressures and uncertainty from global developments.

Market review

Equities

Global equities posted solid returns in May. US large caps performed well, driven by technology and AI-related names that reported strong revenue beats and raised near-term guidance in several cases. Emerging markets also rebounded, led by exporters tied to the semiconductor and electronics supply chain. European and Japanese markets recovered from earlier weakness as signs of de‑escalation in the Middle East eased energy fears mid to late month.

New Zealand shares delivered modest gains in May, supported by a rebound in domestic sentiment and stronger tourist arrivals, although gains were capped by continued concerns over input costs for certain sectors.

Fixed interest

Global sovereign bond yields were mixed across the month. Yields initially rose on robust US data and stronger risk appetite, then eased as geopolitical headlines and softer oil prices pushed investors back into safe‑haven assets at times. The US Treasury curve shifted modestly steeper on balance, reflecting continued confidence in growth and the near‑term re-pricing of terminal policy.

New Zealand government bond yields were relatively stable through May as the RBNZ held rates and local inflation dynamics kept yields anchored. NZ sovereign bonds produced positive returns for the month as yields moved slightly lower into month-end.

Currencies and commodities

The New Zealand dollar traded in a tight range through May, ending the month modestly stronger against the US dollar compared with April. FX moves were driven by relative central bank outlooks, commodity price swings, and seasonal NZ export flows. In mid‑May NZD/USD traded near the 0.58–0.59 range before settling around 0.585 by month-end.

Oil prices corrected sharply from April’s highs. Brent and WTI fell through May—dropping below $100 per barrel toward the end of the month—after a combination of diplomatic progress in the Middle East and inventory data suggested easing immediate supply concerns. The energy-led correction weighed on inflation expectations in commodity‑sensitive regions.

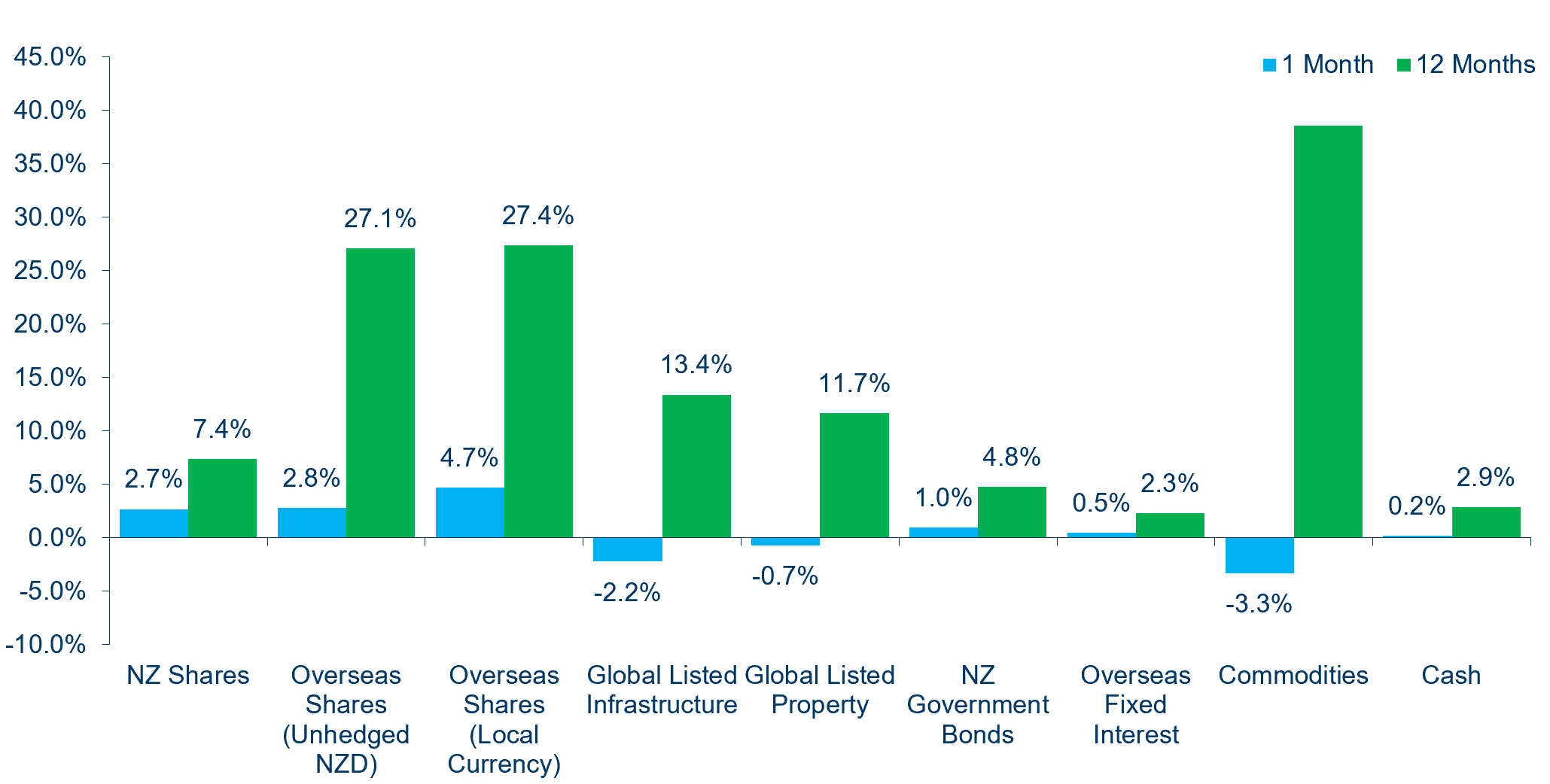

Chart 1: Market returns for periods ending 31 May 2026

Inflation and labour market in New Zealand

New Zealand’s Q1 2026 CPI and business‑survey measures reflected persistent price pressures in housing and utilities. Unemployment remained relatively contained, and labour market tightness in some services sectors continued to support wage growth. The RBNZ’s May statement emphasised a careful balancing act: policy needs to remain sufficiently restrictive to return inflation to target while being mindful of the growth impact of prolonged high rates.

Sector and regional performance highlights

- Technology and consumer discretionary sectors led global gains on strong AI and cyclical demand signals.

- Energy underperformed sharply in May as oil prices retreated from April spikes.

- Defensive sectors (consumer staples, utilities) showed relative strength in intermittent risk‑off windows.

- Emerging market equities outperformed materially in parts of Asia tied to semiconductor exports.

Looking ahead

Risk themes to monitor:

- Trade policy developments: Tariff regimes and bilateral negotiations remain a medium-term risk to trade volumes and margins for multinational firms.

- Geopolitical developments and energy security: Any renewed escalation in the Middle East or elsewhere could quickly reverse the recent decline in oil prices and prompt a re‑pricing of inflation and risk assets.

- Central bank signals: With the US Fed leadership transition and differing trajectories across central banks, markets will closely watch incoming inflation and labour data for signals on the timing and magnitude of any policy moves.

- Corporate earnings updates: Further quarterly reports will test whether May’s strong earnings momentum broadens beyond a handful of large-cap tech firms.

Conclusion

May 2026 delivered a constructive month for risk assets driven by strong corporate earnings and a partial easing of energy risks, but the backdrop remains one of uneven disinflation, active trade-policy risk, and geopolitical fragility. For New Zealand investors, the key local themes are persistent domestic inflationary pressures, and a steady but cautious RBNZ. In environments like this, investors often consider diversification, a focus on quality, and maintaining tactical flexibility to respond rapid policy or geopolitical shifts.

If you’d like to learn more about the Mercer NZ funds on InvestNow, please visit the Mercer landing page on InvestNow.

Signs of Calm as Markets Recover Momentum

Global markets appeared to regain momentum in May, supported by strong earnings and easing geopolitical tensions. While risks remain, the backdrop improved for investors. Del Hart shares what drove markets, what it means, and the key themes to watch next.

Introduction

May 2026 saw global markets resume a risk-on tone after a turbulent period of trade policy and geopolitical uncertainty. Strong corporate earnings – particularly from technology firms exposed to AI demand – together with signs of de‑escalation in some geopolitical flashpoints, supported equity markets. At the same time, energy-market developments and a leadership transition at the US Federal Reserve added fresh sources of volatility and policy uncertainty. Against that backdrop, bond yields moved unevenly, commodity prices fell from April peaks, and the New Zealand economy showed mixed domestic momentum amid sticky inflation.

Economic overview

US trade policy continued to shape market narratives. A series of targeted tariffs introduced earlier in 2025 and 2026 remained in place for several product categories, and ongoing bilateral negotiations produced episodic headlines. Markets reacted more to earnings momentum and geopolitics in May than to fresh tariff shocks, but the lingering tariff regime continues to represent a structural headwind for global trade and supply chains.

The US macro picture remained resilient in aggregate. May was dominated by solid corporate earnings – led by semiconductor and software firms capitalising on AI demand – which helped lift investor sentiment. However, business surveys and some cyclical indicators signalled slowing manufacturing momentum. Inflation dynamics showed regional divergence: services inflation remained persistent in parts of the US, while goods inflation eased as energy prices moderated late in the month.

In China, policymakers maintained an accommodative stance to support growth, while European economies continued to battle soft demand even as fiscal measures in some countries provided a partial offset. Global growth forecasts were nudged modestly higher on resilient activity data, although downside risks from a renewed Middle East energy shock remained present.

New Zealand’s Q1 2026 inflation print confirmed higher-than-expected price pressures, with annual CPI around the low 3% area and notable contributions from housing‑related costs and utilities. Against that backdrop, the RBNZ kept the Official Cash Rate on hold at its May meeting, citing both persistent domestic inflation pressures and uncertainty from global developments.

Market review

Equities

Global equities posted solid returns in May. US large caps performed well, driven by technology and AI-related names that reported strong revenue beats and raised near-term guidance in several cases. Emerging markets also rebounded, led by exporters tied to the semiconductor and electronics supply chain. European and Japanese markets recovered from earlier weakness as signs of de‑escalation in the Middle East eased energy fears mid to late month.

New Zealand shares delivered modest gains in May, supported by a rebound in domestic sentiment and stronger tourist arrivals, although gains were capped by continued concerns over input costs for certain sectors.

Fixed interest

Global sovereign bond yields were mixed across the month. Yields initially rose on robust US data and stronger risk appetite, then eased as geopolitical headlines and softer oil prices pushed investors back into safe‑haven assets at times. The US Treasury curve shifted modestly steeper on balance, reflecting continued confidence in growth and the near‑term re-pricing of terminal policy.

New Zealand government bond yields were relatively stable through May as the RBNZ held rates and local inflation dynamics kept yields anchored. NZ sovereign bonds produced positive returns for the month as yields moved slightly lower into month-end.

Currencies and commodities

The New Zealand dollar traded in a tight range through May, ending the month modestly stronger against the US dollar compared with April. FX moves were driven by relative central bank outlooks, commodity price swings, and seasonal NZ export flows. In mid‑May NZD/USD traded near the 0.58–0.59 range before settling around 0.585 by month-end.

Oil prices corrected sharply from April’s highs. Brent and WTI fell through May—dropping below $100 per barrel toward the end of the month—after a combination of diplomatic progress in the Middle East and inventory data suggested easing immediate supply concerns. The energy-led correction weighed on inflation expectations in commodity‑sensitive regions.

Chart 1: Market returns for periods ending 31 May 2026

Inflation and labour market in New Zealand

New Zealand’s Q1 2026 CPI and business‑survey measures reflected persistent price pressures in housing and utilities. Unemployment remained relatively contained, and labour market tightness in some services sectors continued to support wage growth. The RBNZ’s May statement emphasised a careful balancing act: policy needs to remain sufficiently restrictive to return inflation to target while being mindful of the growth impact of prolonged high rates.

Sector and regional performance highlights

- Technology and consumer discretionary sectors led global gains on strong AI and cyclical demand signals.

- Energy underperformed sharply in May as oil prices retreated from April spikes.

- Defensive sectors (consumer staples, utilities) showed relative strength in intermittent risk‑off windows.

- Emerging market equities outperformed materially in parts of Asia tied to semiconductor exports.

Looking ahead

Risk themes to monitor:

- Trade policy developments: Tariff regimes and bilateral negotiations remain a medium-term risk to trade volumes and margins for multinational firms.

- Geopolitical developments and energy security: Any renewed escalation in the Middle East or elsewhere could quickly reverse the recent decline in oil prices and prompt a re‑pricing of inflation and risk assets.

- Central bank signals: With the US Fed leadership transition and differing trajectories across central banks, markets will closely watch incoming inflation and labour data for signals on the timing and magnitude of any policy moves.

- Corporate earnings updates: Further quarterly reports will test whether May’s strong earnings momentum broadens beyond a handful of large-cap tech firms.

Conclusion

May 2026 delivered a constructive month for risk assets driven by strong corporate earnings and a partial easing of energy risks, but the backdrop remains one of uneven disinflation, active trade-policy risk, and geopolitical fragility. For New Zealand investors, the key local themes are persistent domestic inflationary pressures, and a steady but cautious RBNZ. In environments like this, investors often consider diversification, a focus on quality, and maintaining tactical flexibility to respond rapid policy or geopolitical shifts.

If you’d like to learn more about the Mercer NZ funds on InvestNow, please visit the Mercer landing page on InvestNow.

Leave A Comment