InvestNow News – 10th July – Milford – Health Care: A hunting ground for investment opportunities in uncertain times

Article written by Alexander Whight, Milford – 1st July

It is hard to believe just 3 months have passed since the market lows of late-March. Equity markets have moved quickly to price an economic recovery as countries around the world reopen and authorities step up with record fiscal and monetary policy support. But how sustainable is this improvement? The pandemic is far from over and the saddening human cost mounting. Significant capital is being invested in the search for a vaccine and to improve hospital care for the unfortunate who contract COVID-19. The outlook for markets is uncertain, leaving us seeking portfolio balance. This can partly be achieved with a “barbell” approach, balancing recovery plays with defensive positions and pandemic beneficiaries. Healthcare is a home for companies that may offer us a bit of both.

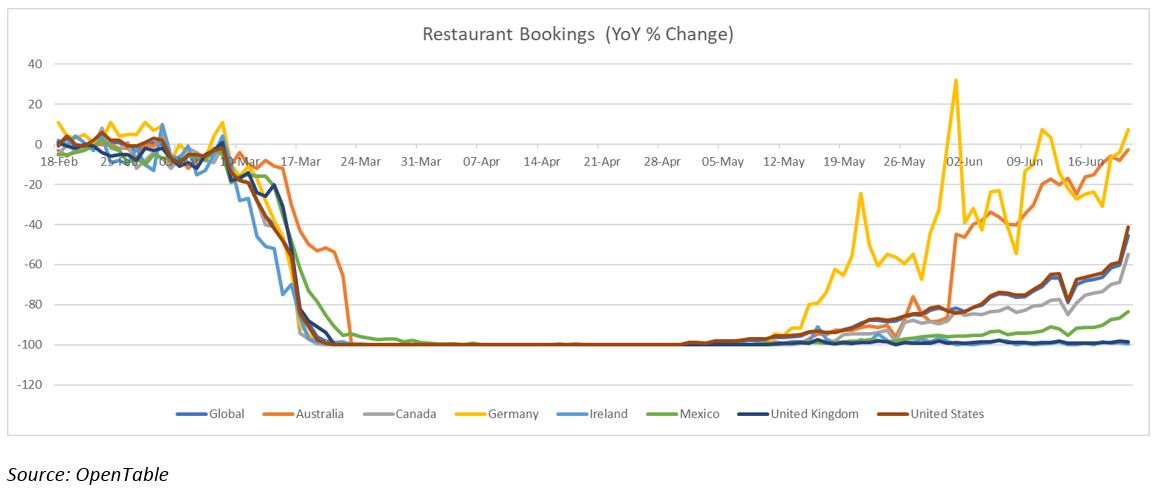

It is no surprise to see improvements in consumer and industrial activity as restrictions ease. Countries were in lockdown, with industries closing-up shop almost overnight, inflicting significant social costs on society. Hospitality and tourism have been severely disrupted. Restaurants went to zero and, whilst now recovering, remain severely depressed. Small businesses need community support; we implore those fortunate enough to afford to eat out or holiday to do just that. Get to the barber or beautician for some post-isolation grooming. Shop local. Maintain vigilance. We can all play a part.

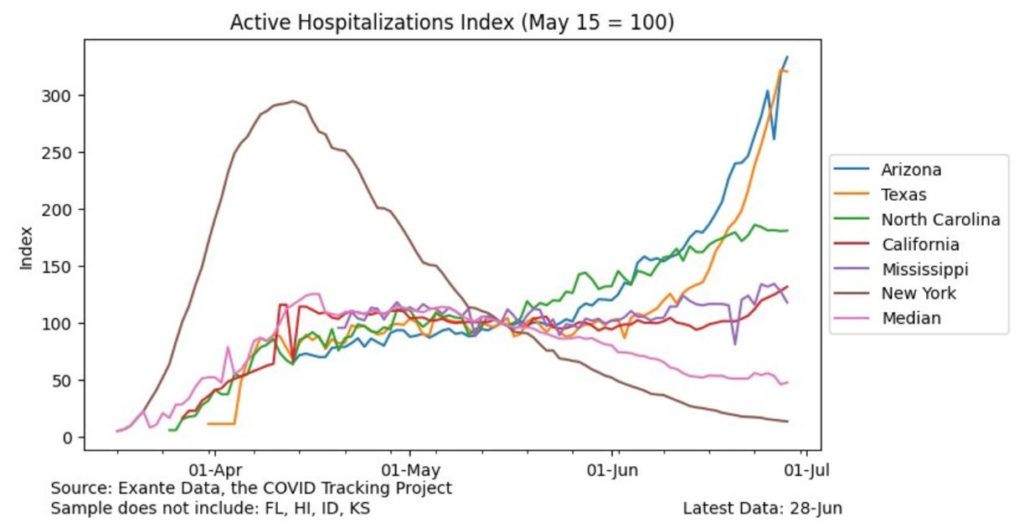

When considering the strength and duration of a recovery we find ourselves faced with many questions. One is, how will communities and governments react to any “second wave” of COVID-19 cases? New COVID-19 cases are inevitable as economies reopen, but we expect, and observe, a reluctance from governments to reimpose wide-scale lockdowns. Lockdowns should be localised and a last resort. As we are seeing in the USA, a limiting factor to this approach is health care system capacity. Hospitalisation rates in US states where cases are rising do suggest a risk that future restrictions are imposed. Intensive care utilisation is virtually at capacity in Texas, 88% in Arizona (~60% pre-crisis), and 76% in Florida.

Importantly, hospitals do appear better-prepared, having had time to build capability, including inventory of critical medical devices and other items. This has been a boon for the world’s largest disposable glove manufacturer, Top Glove (listed in Malaysia), which from pre-pandemic levels has seen sales rise >35% and profit margins more than double amidst surging demand and strong price increases. The stock has responded accordingly, up >3x in 2020. We question how sustainable Top Glove’s increase in profits will prove to be and instead seek out companies like California’s Masimo Corp., which is an important part of the COVID-19 response and, post-pandemic, stands to emerge a stronger company.

The COVID-19 response has increased demand for Masimo’s pulse oximetry solutions, which non-invasively monitor a patient’s vital signs. Masimo is the clear technology leader, a giant in this niche market. Some of this demand will normalise post-pandemic but dealing with the outbreak is driving hospitals to adopt other Masimo solutions. Hospitals are using Masimo’s wireless solutions to remotely monitor patients’ vital signs in the hospital ward or even at home, without regularly coming into physical contact with patients. This reduces disease transmission and frees up important hospital capacity for those that need more acute care. Importantly, in a “normal” hospital operating environment these same solutions improve the quality of health care and reduce system costs. Increased customer familiarity induced by the pandemic bodes well for long-term demand for Masimo’s products.

The health care sector is critical to managing our way through the pandemic and is opportunity-rich from an investment perspective. Masimo is not alone and we continue our research efforts in this dynamic space.

Disclosure of interest: Milford holds shares in Masimo on behalf of clients.

Disclaimer: The material contained herein is based on information believed to be accurate and reliable although no guarantee can be given that this is the case. This is intended to provide general information only. It does not take into account your investment needs or personal circumstances. It is not intended to be viewed as investment or financial advice. Before making any financial decisions, you may wish to seek independent financial advice.

InvestNow News – 10th July – Milford – Health Care: A hunting ground for investment opportunities in uncertain times

Article written by Alexander Whight, Milford – 1st July

It is hard to believe just 3 months have passed since the market lows of late-March. Equity markets have moved quickly to price an economic recovery as countries around the world reopen and authorities step up with record fiscal and monetary policy support. But how sustainable is this improvement? The pandemic is far from over and the saddening human cost mounting. Significant capital is being invested in the search for a vaccine and to improve hospital care for the unfortunate who contract COVID-19. The outlook for markets is uncertain, leaving us seeking portfolio balance. This can partly be achieved with a “barbell” approach, balancing recovery plays with defensive positions and pandemic beneficiaries. Healthcare is a home for companies that may offer us a bit of both.

It is no surprise to see improvements in consumer and industrial activity as restrictions ease. Countries were in lockdown, with industries closing-up shop almost overnight, inflicting significant social costs on society. Hospitality and tourism have been severely disrupted. Restaurants went to zero and, whilst now recovering, remain severely depressed. Small businesses need community support; we implore those fortunate enough to afford to eat out or holiday to do just that. Get to the barber or beautician for some post-isolation grooming. Shop local. Maintain vigilance. We can all play a part.

When considering the strength and duration of a recovery we find ourselves faced with many questions. One is, how will communities and governments react to any “second wave” of COVID-19 cases? New COVID-19 cases are inevitable as economies reopen, but we expect, and observe, a reluctance from governments to reimpose wide-scale lockdowns. Lockdowns should be localised and a last resort. As we are seeing in the USA, a limiting factor to this approach is health care system capacity. Hospitalisation rates in US states where cases are rising do suggest a risk that future restrictions are imposed. Intensive care utilisation is virtually at capacity in Texas, 88% in Arizona (~60% pre-crisis), and 76% in Florida.

Importantly, hospitals do appear better-prepared, having had time to build capability, including inventory of critical medical devices and other items. This has been a boon for the world’s largest disposable glove manufacturer, Top Glove (listed in Malaysia), which from pre-pandemic levels has seen sales rise >35% and profit margins more than double amidst surging demand and strong price increases. The stock has responded accordingly, up >3x in 2020. We question how sustainable Top Glove’s increase in profits will prove to be and instead seek out companies like California’s Masimo Corp., which is an important part of the COVID-19 response and, post-pandemic, stands to emerge a stronger company.

The COVID-19 response has increased demand for Masimo’s pulse oximetry solutions, which non-invasively monitor a patient’s vital signs. Masimo is the clear technology leader, a giant in this niche market. Some of this demand will normalise post-pandemic but dealing with the outbreak is driving hospitals to adopt other Masimo solutions. Hospitals are using Masimo’s wireless solutions to remotely monitor patients’ vital signs in the hospital ward or even at home, without regularly coming into physical contact with patients. This reduces disease transmission and frees up important hospital capacity for those that need more acute care. Importantly, in a “normal” hospital operating environment these same solutions improve the quality of health care and reduce system costs. Increased customer familiarity induced by the pandemic bodes well for long-term demand for Masimo’s products.

The health care sector is critical to managing our way through the pandemic and is opportunity-rich from an investment perspective. Masimo is not alone and we continue our research efforts in this dynamic space.

Disclosure of interest: Milford holds shares in Masimo on behalf of clients.

Disclaimer: The material contained herein is based on information believed to be accurate and reliable although no guarantee can be given that this is the case. This is intended to provide general information only. It does not take into account your investment needs or personal circumstances. It is not intended to be viewed as investment or financial advice. Before making any financial decisions, you may wish to seek independent financial advice.