InvestNow News – 8th October – Franklin Templeton – The Great Reckoning—Reflecting on the Evergrande Saga

Article written by Tracy Chen, CFA, CAIA, Portfolio Manager, Franklin Templeton – 23rd September 2021

Brandywine Global: China’s economic growth deceleration has been of increasing concern to global markets. The Evergrande crisis has brought these worries to a flashpoint.

China’s economic growth deceleration, triggered by a zero-COVID-19 policy and multi-faceted regulatory tightening, has been of increasing concern to global markets. Removing excesses and improving the health of the property sector have been objectives of the more stringent regulatory environment, but these efforts have resulted in acute financial duress for Evergrande, one of the China’s largest and most indebted property developers. The Evergrande crisis, an epitome of China’s great reckoning following its go-go growth days, has brought these worries to a flashpoint. We do not believe Evergrande is a black swan event— it has been brewing for several years, eliminating the element of surprise. Instead, it could be a “grey rhino,” a highly probable event with a potentially profound impact, if not handled with caution in a timely manner. Evergrande has a large footprint, including multiple business lines, a vast number of stakeholders, and thousands of upstream and downstream partners. Further complicating matters are the opaqueness of its shadow lending and the intertwined financial web linkages. The key risk is whether policymakers can contain the impact of an Evergrande default to avoid a broad-based credit/liquidity crunch. Otherwise, the potential ramifications may include a significant loss of confidence, economic downturn, or financial instability. The People’s Bank of China (PBOC) has been injecting liquidity into the system to prevent a market liquidity squeeze. Shoring up investor confidence is critical. The refinancing of other property developer bonds will be challenging if this rout is not stopped in an orderly manner.

Shift of Policy Focus

The trade war and COVID-19 have necessitated that Chinese policymakers consider a shift in policy to pursue more self-sufficient and sustainable growth. The top three priorities for the Chinese government are:

- Tackling high levels of debt

- Arresting deteriorating demographics

- Boosting labor productivity

High property prices have been squeezing the middle class, discouraging fertility, and widening the wealth gap. Meanwhile, the introduction of China’s “three red lines” deleveraging campaign in August 2020, aimed at improving the financial health of the real estate sector, has been the inflection point that exacerbated Evergrande’s woes. However, property market tightening could achieve a trifecta: tightening credit to property developers and mortgage lending, stabilizing property and land prices as well as price expectations, and channeling capital away from the unproductive property sector to more productive sectors (see Chart 1).

China’s Property Sector Has Slowed Due to Bank Lending Squeeze

% YoY, As of Q2 2021

Source: Brandywine Global, Macrobond, PBOC

Evergrande expanded aggressively since the early 2000s to become one of China’s largest and most levered property developers. Currently, it has over RMB 2 trillion ($300 billion) in liabilities on its balance sheet with very limited cash. However, Evergrande’s credit woes are not news. Its stock price has been on a downtrend since its peak in 2017. Since February 2021, the deterioration accelerated as the “three red lines” regulations intensified (see Chart 2). Now, Evergrande is experiencing acute liquidity risk with difficulty meeting its operational obligations and coupon payments.

Evergrande Equity (HKD) and Bond Prices (USD)

Last Price, As of 9/21/2021

Source: Bloomberg (© 2021, Bloomberg Finance LP)

Contagion Risks

There are multiple possible contagion effects that investors must assess. A disorderly credit event related to Evergrande could lead to the broadening of social and financial risks.

- The contagion effect on financial markets so far can be seen in the underperformance of equities and bonds of property developers. However, there is almost no sign of a liquidity squeeze in China’s interbank market, with SHIBOR and 7-day repo rates very stable. The global selloff in risk assets on September 20, 2021, was a delayed broadening of the contagion risk.

- Another nuance of the contagion effect on financial markets is the exposure of China’s banking system to Evergrande. Evergrande’s liabilities represent around 0.6% of China’s bank assets. National joint-stock banks, including Minsheng Bank, have larger exposure to Evergrande while China’s Big Four banks have less exposure. Hence, a systemic banking crisis does not seem likely. However, policymakers need to ensure that they can quarantine the Evergrande crisis to avoid widespread default of other weaker developers.

- The social contagion effect relates to the ability to ensure ongoing project delivery to buyers and payments to project partners. Among Evergrande’s RMB 2 trillion liabilities, RMB 1 trillion represents trade payables to more than 8,000 upstream and downstream partners. Defaulting on the payables could cause financial distress at these trade partners. Furthermore, unfinished projects in more than 220 cities and to nearly 2 million homebuyers present risks to social stability. Recent protests demonstrate the importance to social stability.

- The current crisis may cause homebuyers to delay home purchases, impacting the real economy by lowering property sales and prices, land sales and prices, and construction investments, and by weakening upstream and downstream industries as well as commodity prices. As Evergrande and other weak property developers try to sell assets quickly to raise cash and cover liabilities, property prices could take a further hit. Nevertheless, the macroeconomic impact from the worst-case contagion effect would likely be smaller than the 2014 – 2015 property downturn as current property inventories remain low (see Chart 3). In the case of a sharper property correction, we would expect both fiscal and monetary policies to ease further, and there may be some modest adjustment in property policies as well.

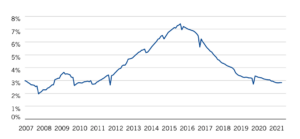

Chinese Property Inventory Is Lower than in 2015

Unsold Floor Space of Residential Buildings, % of Total, As of 7/31/2021

Source: Haver Analytics

Policy Options to Contain the Contagion

We need to keep in mind that the Evergrande crisis was a side effect of policymakers looking to rein in a reckless credit binge and punish bad actors in China’s property market. Policymakers need to balance attacking the moral hazard of “too big to fail” with also containing systemic risk. We believe policy measures will be launched in the next few weeks to calm the market, arrest the sharp growth slowdown, and mitigate financial risks. Those measures could include injecting more liquidity into the financial system, more local special government bond issuance, reserve requirement ratio (RRR) cuts, fine-tuning property market tightening, loosening COVID-19 restrictions, and easing decarbonization-driven production cuts, among other actions.

Investment Implications

The Evergrande crisis is a deflationary shock to the Chinese economy, even though we do believe Chinese policymakers have the wherewithal to avoid a systemic risk. Our base case would be an orderly restructuring of Evergrande that potentially may include splitting the conglomerate into several parts. This restructuring may be followed by some state-owned enterprises (SOE) taking over unfinished projects and operational liabilities, combined with debt term extension and sale of assets to other developers. In times of default or distress, investors of offshore property developer bonds need to be cognizant of the payment pecking order. Obligations to homebuyers and suppliers will take priority, followed by claims by banks, onshore bondholders, offshore bondholders, and equity owners. Different claims of asset recovery and covenant structure between onshore and offshore bond holders are also very important.

China’s policy easing is becoming more nuanced and targeted given its policy focus shift, and it needs to reserve some room for next year should the economy weaken more. The fiscal impulse is in the bottoming process with government bond issuance picking up in the third quarter. However, with that being said, there is always a risk that policymakers act too late or too little. In that case, the impact of the sharp slowdown on global growth and risk assets could be quite negative until we see decisive easing measures in a timely manner. Under this scenario, China-centric commodity prices will be under tremendous pressure; Chinese government bonds should still do well as a result of the flight to quality; the onshore renminbi (CNY) and the offshore renminbi (CNH) will experience some pressure from the growth slowdown and potential uptick in capital outflows; and there will be more pain in the property sector with bouts of market volatility. It will not be an easy task to select winners from losers with the macro uncertainty and potential contagion risks, and the ride likely will not be smooth. However, we believe the current environment presents a compelling valuation opportunity to take advantage of market dislocations, although we would emphasize that investors should be highly selective and focus on buying quality names.

DEFINITIONS:

A black swan event, in the world of finance, is an extremely negative event or occurrence that is impossibly difficult to predict.

In August 2020, China announced “Three red lines,” guidelines to encourage developers to deleverage. The rules set limits for three financial ratios that determine a developer’s future borrowing growth rate. For developers who meet all three limits (coded green), annual borrowing growth is capped at 15%. Developers who breach all three limits (coded red) face zero growth in total borrowing.

Fiscal impulse is a measure of change in the government budget balance resulting from changes in government expenditure and tax policies.

The reserve requirement ratio (RRR) is the percentage of depositors’ balances banks must have on hand as cash.

The Shanghai Interbank Offered Rate (SHIBOR) is a daily reference rate based on the interest rates at which banks offer to lend unsecured funds to other banks in the Shanghai wholesale (or “interbank”) money market.

Onshore renminbi CNY is the currency used in China, and CNH is the offshore currency. The value of CNY is controlled by the Chinese government. The central bank, the People’s Bank of China, publishes a reference rate for the currency each day. On the other hand, CNH is traded freely in global markets, and its value changes based on the market.

WHAT ARE THE RISKS?

Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

U.S. Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the U.S. government. The U.S. government guarantees the principal and interest payments on U.S. Treasuries when the securities are held to maturity. Unlike U.S. Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the U.S. government. Even when the U.S. government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe’s website.

Franklin Templeton Distributors, Inc.

InvestNow News – 8th October – Franklin Templeton – The Great Reckoning—Reflecting on the Evergrande Saga

Article written by Tracy Chen, CFA, CAIA, Portfolio Manager, Franklin Templeton – 23rd September 2021

Brandywine Global: China’s economic growth deceleration has been of increasing concern to global markets. The Evergrande crisis has brought these worries to a flashpoint.

China’s economic growth deceleration, triggered by a zero-COVID-19 policy and multi-faceted regulatory tightening, has been of increasing concern to global markets. Removing excesses and improving the health of the property sector have been objectives of the more stringent regulatory environment, but these efforts have resulted in acute financial duress for Evergrande, one of the China’s largest and most indebted property developers. The Evergrande crisis, an epitome of China’s great reckoning following its go-go growth days, has brought these worries to a flashpoint. We do not believe Evergrande is a black swan event— it has been brewing for several years, eliminating the element of surprise. Instead, it could be a “grey rhino,” a highly probable event with a potentially profound impact, if not handled with caution in a timely manner. Evergrande has a large footprint, including multiple business lines, a vast number of stakeholders, and thousands of upstream and downstream partners. Further complicating matters are the opaqueness of its shadow lending and the intertwined financial web linkages. The key risk is whether policymakers can contain the impact of an Evergrande default to avoid a broad-based credit/liquidity crunch. Otherwise, the potential ramifications may include a significant loss of confidence, economic downturn, or financial instability. The People’s Bank of China (PBOC) has been injecting liquidity into the system to prevent a market liquidity squeeze. Shoring up investor confidence is critical. The refinancing of other property developer bonds will be challenging if this rout is not stopped in an orderly manner.

Shift of Policy Focus

The trade war and COVID-19 have necessitated that Chinese policymakers consider a shift in policy to pursue more self-sufficient and sustainable growth. The top three priorities for the Chinese government are:

- Tackling high levels of debt

- Arresting deteriorating demographics

- Boosting labor productivity

High property prices have been squeezing the middle class, discouraging fertility, and widening the wealth gap. Meanwhile, the introduction of China’s “three red lines” deleveraging campaign in August 2020, aimed at improving the financial health of the real estate sector, has been the inflection point that exacerbated Evergrande’s woes. However, property market tightening could achieve a trifecta: tightening credit to property developers and mortgage lending, stabilizing property and land prices as well as price expectations, and channeling capital away from the unproductive property sector to more productive sectors (see Chart 1).

China’s Property Sector Has Slowed Due to Bank Lending Squeeze

% YoY, As of Q2 2021

Source: Brandywine Global, Macrobond, PBOC

Evergrande expanded aggressively since the early 2000s to become one of China’s largest and most levered property developers. Currently, it has over RMB 2 trillion ($300 billion) in liabilities on its balance sheet with very limited cash. However, Evergrande’s credit woes are not news. Its stock price has been on a downtrend since its peak in 2017. Since February 2021, the deterioration accelerated as the “three red lines” regulations intensified (see Chart 2). Now, Evergrande is experiencing acute liquidity risk with difficulty meeting its operational obligations and coupon payments.

Evergrande Equity (HKD) and Bond Prices (USD)

Last Price, As of 9/21/2021

Source: Bloomberg (© 2021, Bloomberg Finance LP)

Contagion Risks

There are multiple possible contagion effects that investors must assess. A disorderly credit event related to Evergrande could lead to the broadening of social and financial risks.

- The contagion effect on financial markets so far can be seen in the underperformance of equities and bonds of property developers. However, there is almost no sign of a liquidity squeeze in China’s interbank market, with SHIBOR and 7-day repo rates very stable. The global selloff in risk assets on September 20, 2021, was a delayed broadening of the contagion risk.

- Another nuance of the contagion effect on financial markets is the exposure of China’s banking system to Evergrande. Evergrande’s liabilities represent around 0.6% of China’s bank assets. National joint-stock banks, including Minsheng Bank, have larger exposure to Evergrande while China’s Big Four banks have less exposure. Hence, a systemic banking crisis does not seem likely. However, policymakers need to ensure that they can quarantine the Evergrande crisis to avoid widespread default of other weaker developers.

- The social contagion effect relates to the ability to ensure ongoing project delivery to buyers and payments to project partners. Among Evergrande’s RMB 2 trillion liabilities, RMB 1 trillion represents trade payables to more than 8,000 upstream and downstream partners. Defaulting on the payables could cause financial distress at these trade partners. Furthermore, unfinished projects in more than 220 cities and to nearly 2 million homebuyers present risks to social stability. Recent protests demonstrate the importance to social stability.

- The current crisis may cause homebuyers to delay home purchases, impacting the real economy by lowering property sales and prices, land sales and prices, and construction investments, and by weakening upstream and downstream industries as well as commodity prices. As Evergrande and other weak property developers try to sell assets quickly to raise cash and cover liabilities, property prices could take a further hit. Nevertheless, the macroeconomic impact from the worst-case contagion effect would likely be smaller than the 2014 – 2015 property downturn as current property inventories remain low (see Chart 3). In the case of a sharper property correction, we would expect both fiscal and monetary policies to ease further, and there may be some modest adjustment in property policies as well.

Chinese Property Inventory Is Lower than in 2015

Unsold Floor Space of Residential Buildings, % of Total, As of 7/31/2021

Source: Haver Analytics

Policy Options to Contain the Contagion

We need to keep in mind that the Evergrande crisis was a side effect of policymakers looking to rein in a reckless credit binge and punish bad actors in China’s property market. Policymakers need to balance attacking the moral hazard of “too big to fail” with also containing systemic risk. We believe policy measures will be launched in the next few weeks to calm the market, arrest the sharp growth slowdown, and mitigate financial risks. Those measures could include injecting more liquidity into the financial system, more local special government bond issuance, reserve requirement ratio (RRR) cuts, fine-tuning property market tightening, loosening COVID-19 restrictions, and easing decarbonization-driven production cuts, among other actions.

Investment Implications

The Evergrande crisis is a deflationary shock to the Chinese economy, even though we do believe Chinese policymakers have the wherewithal to avoid a systemic risk. Our base case would be an orderly restructuring of Evergrande that potentially may include splitting the conglomerate into several parts. This restructuring may be followed by some state-owned enterprises (SOE) taking over unfinished projects and operational liabilities, combined with debt term extension and sale of assets to other developers. In times of default or distress, investors of offshore property developer bonds need to be cognizant of the payment pecking order. Obligations to homebuyers and suppliers will take priority, followed by claims by banks, onshore bondholders, offshore bondholders, and equity owners. Different claims of asset recovery and covenant structure between onshore and offshore bond holders are also very important.

China’s policy easing is becoming more nuanced and targeted given its policy focus shift, and it needs to reserve some room for next year should the economy weaken more. The fiscal impulse is in the bottoming process with government bond issuance picking up in the third quarter. However, with that being said, there is always a risk that policymakers act too late or too little. In that case, the impact of the sharp slowdown on global growth and risk assets could be quite negative until we see decisive easing measures in a timely manner. Under this scenario, China-centric commodity prices will be under tremendous pressure; Chinese government bonds should still do well as a result of the flight to quality; the onshore renminbi (CNY) and the offshore renminbi (CNH) will experience some pressure from the growth slowdown and potential uptick in capital outflows; and there will be more pain in the property sector with bouts of market volatility. It will not be an easy task to select winners from losers with the macro uncertainty and potential contagion risks, and the ride likely will not be smooth. However, we believe the current environment presents a compelling valuation opportunity to take advantage of market dislocations, although we would emphasize that investors should be highly selective and focus on buying quality names.

DEFINITIONS:

A black swan event, in the world of finance, is an extremely negative event or occurrence that is impossibly difficult to predict.

In August 2020, China announced “Three red lines,” guidelines to encourage developers to deleverage. The rules set limits for three financial ratios that determine a developer’s future borrowing growth rate. For developers who meet all three limits (coded green), annual borrowing growth is capped at 15%. Developers who breach all three limits (coded red) face zero growth in total borrowing.

Fiscal impulse is a measure of change in the government budget balance resulting from changes in government expenditure and tax policies.

The reserve requirement ratio (RRR) is the percentage of depositors’ balances banks must have on hand as cash.

The Shanghai Interbank Offered Rate (SHIBOR) is a daily reference rate based on the interest rates at which banks offer to lend unsecured funds to other banks in the Shanghai wholesale (or “interbank”) money market.

Onshore renminbi CNY is the currency used in China, and CNH is the offshore currency. The value of CNY is controlled by the Chinese government. The central bank, the People’s Bank of China, publishes a reference rate for the currency each day. On the other hand, CNH is traded freely in global markets, and its value changes based on the market.

WHAT ARE THE RISKS?

Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

U.S. Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the U.S. government. The U.S. government guarantees the principal and interest payments on U.S. Treasuries when the securities are held to maturity. Unlike U.S. Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the U.S. government. Even when the U.S. government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe’s website.

Franklin Templeton Distributors, Inc.