InvestNow News – 5th March – Russell Investments – DB plan hibernation: Does it really work?

Article written by Justin Owens, Russell Investments – 24th February 2021

Nearly five years have passed since we first issued our guide to pension plan hibernation. Since that time, this concept has resonated across our client base and in the pension industry.

Plan hibernation does not ignore that a closed and frozen defined benefit (DB) plan will eventually terminate. Plan hibernation simply holds the plan in a risk-mitigating position to “do no harm” to the sponsor by maintaining its fully funded position. Doing so allows the plan to continue to mature on its own, naturally defeasing a significant portion of liabilities through benefit payments, and reducing the ultimate cost of termination.

But does plan hibernation really work? We have some actual client experience to help answer that question.

Plan hibernation – quick refresher

![]()

Every DB plan has a lifecycle. At one point, each of them was open and ongoing. Over time, many sponsors have chosen to close and/or freeze their plan. This kicked off the next stage in their lifecycle, where the participant base is static and ultimately (for frozen plans) the benefits are set as well. At this stage a glidepath is usually adopted, gradually reducing risk by incrementally shifting the asset allocation as funded status improves.

Once a plan reaches a desired funded position %, the hibernation can ensue by adopting an asset allocation designed to maintain its funded position. This usually means 80-90% allocated to liability-hedging fixed income, typically accompanied by a small allocation to return-seeking assets to generate sufficient return to overcome any funded status headwinds that may arise, such as ongoing expenses paid from plan assets, potential actuarial losses, as well as credit migration within fixed income assets (i.e., defaults/downgrades).

Regardless of the future path of interest rates, credit spreads and equity returns, the funded status of a hibernating plan (with an appropriate asset allocation strategy) should hold reasonably steady, thus avoiding PBGC variable rate premiums and contribution requirements. Sponsors usually still pay ongoing plan expenses (e.g., actuarial fees, investments management, PBGC flat rate premiums, etc.) out of plan assets, thus leaving few expenses to be paid by the sponsor.

Over time, the size of a plan’s liabilities declines as participants age, particularly as they retire and draw benefits then ultimately pass on. In our experience, a sponsor of a frozen plan can expect the plan liabilities to fall by up to 1/3 over a ten-year period by natural attrition, and potentially significantly more in some cases depending on the cash flow profile of the plan. This lowers the cost of a plan termination due to the plan’s smaller size, and the fact that retirees are the least expensive group to annuitize. Purchasing annuities for non-retired groups can be very expensive due to the added uncertainty of their future benefits timing.

While a plan is in hibernation, risk transfer may be pursued, such as for retirees with small benefits or lump sum cashouts to terminated vested participants. But the sponsor should only pursue these transactions if they result in savings to the sponsor and should be considered opportunistically.

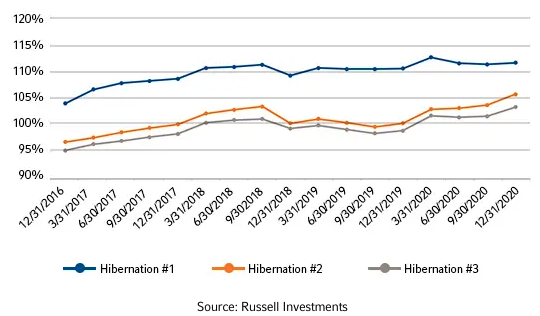

Case Studies – has funded status been maintained?

The proposition of hibernation sounds appealing to plan sponsors, but some may still question if the plan’s funded status can really be maintained, especially after a year like 2020 with extreme volatility in the first quarter. The effects of plan expenses, credit migration and periodic actuarial adjustments can create drag on funded status, so what has been the actual experience for plans in hibernation?

In the exhibit below, we show the actual experience of three plans that adopted a hibernation as they approached a fully funded position. Each plan had an asset allocation containing 85%+ in high quality fixed income and reallocated these LDI assets every year based on updated actuarial cash flows and the current market environment. This is standard practice for any of our clients in hibernation.

In the lower two lines, you’ll notice they adopted their hibernation asset allocation even before they were fully funded. None of these sponsors made any contributions over the horizon, and plan expenses (including PBGC premiums, actuarial fees and investment management fees) were paid from plan assets.

Evolution of funded status

12/31/2016 – 12/31/2020

For each of these plans, the funded status has been steady over time. Note that despite multiple periods where funded status was severely challenged in the DB industry at large, the funded status of these plans have remained fairly consistent. Ironically, funded status actually increased in Q1 2020 during the recent COVID-related turmoil. These are just three actual examples of how the hibernation strategy can work if properly executed.

Common concerns with hibernation

Some may question of the merits of hibernation on the following grounds. We’d like to address each of them.

PV of future expenses: some argue that the present value of future expenses required by DB plans justifies paying an additional premium to an insurance company to annuitize the plan. However, if the plan assets generate sufficient return to compensate for these expenses directly (as our real life examples demonstrate), the sponsor will not be required to make contributions to cover them.

Credit migration: we have demonstrated repeatedly with our clients that the effects of defaults and downgrades can be significantly reduced through an effective LDI strategy and composition, alongside skilled investment management.

Actuarial gains/losses: plan hibernation is not designed to directly hedge against actuarial losses. Actuarial valuations should be unbiased and thus lead to similar potential for actuarial gains as much as losses, but a sponsor can only hedge this risk completely through insurance products. For this reason, we typically advocate building in a small funded status buffer above accounting liability at the outset of hibernation to help protect funded status in the case that assumptions used by the plan’s actuary are not aligned with future experience. Nevertheless, even if the funded status is impacted by such actuarial losses over the short term, contributions are unlikely to be required under current funding rules, allowing time for the funded status to recover.

Of course, while our actual client experience with hibernation strategies has been positive, other sponsors that are unable or unwilling to take any of these risks may deem the insurance premium required for full plan termination to be worth the expense. But the majority of plan sponsors appreciate the flexibility plan hibernation offers, until the financial and administrative timing of full plan termination is appropriate.

Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Russell Investments is the owner of the trademarks, service marks, and copyrights related to its respective indexes. Investments in products based on the Russell indexes may not provide the exact performance of the index due to implementation strategies, expenses and fees applicable to the investment product.

The Russell Investments logo is a trademark and service mark of Russell Investments.

AI-28684

InvestNow News – 5th March – Russell Investments – DB plan hibernation: Does it really work?

Article written by Justin Owens, Russell Investments – 24th February 2021

Nearly five years have passed since we first issued our guide to pension plan hibernation. Since that time, this concept has resonated across our client base and in the pension industry.

Plan hibernation does not ignore that a closed and frozen defined benefit (DB) plan will eventually terminate. Plan hibernation simply holds the plan in a risk-mitigating position to “do no harm” to the sponsor by maintaining its fully funded position. Doing so allows the plan to continue to mature on its own, naturally defeasing a significant portion of liabilities through benefit payments, and reducing the ultimate cost of termination.

But does plan hibernation really work? We have some actual client experience to help answer that question.

Plan hibernation – quick refresher

![]()

Every DB plan has a lifecycle. At one point, each of them was open and ongoing. Over time, many sponsors have chosen to close and/or freeze their plan. This kicked off the next stage in their lifecycle, where the participant base is static and ultimately (for frozen plans) the benefits are set as well. At this stage a glidepath is usually adopted, gradually reducing risk by incrementally shifting the asset allocation as funded status improves.

Once a plan reaches a desired funded position %, the hibernation can ensue by adopting an asset allocation designed to maintain its funded position. This usually means 80-90% allocated to liability-hedging fixed income, typically accompanied by a small allocation to return-seeking assets to generate sufficient return to overcome any funded status headwinds that may arise, such as ongoing expenses paid from plan assets, potential actuarial losses, as well as credit migration within fixed income assets (i.e., defaults/downgrades).

Regardless of the future path of interest rates, credit spreads and equity returns, the funded status of a hibernating plan (with an appropriate asset allocation strategy) should hold reasonably steady, thus avoiding PBGC variable rate premiums and contribution requirements. Sponsors usually still pay ongoing plan expenses (e.g., actuarial fees, investments management, PBGC flat rate premiums, etc.) out of plan assets, thus leaving few expenses to be paid by the sponsor.

Over time, the size of a plan’s liabilities declines as participants age, particularly as they retire and draw benefits then ultimately pass on. In our experience, a sponsor of a frozen plan can expect the plan liabilities to fall by up to 1/3 over a ten-year period by natural attrition, and potentially significantly more in some cases depending on the cash flow profile of the plan. This lowers the cost of a plan termination due to the plan’s smaller size, and the fact that retirees are the least expensive group to annuitize. Purchasing annuities for non-retired groups can be very expensive due to the added uncertainty of their future benefits timing.

While a plan is in hibernation, risk transfer may be pursued, such as for retirees with small benefits or lump sum cashouts to terminated vested participants. But the sponsor should only pursue these transactions if they result in savings to the sponsor and should be considered opportunistically.

Case Studies – has funded status been maintained?

The proposition of hibernation sounds appealing to plan sponsors, but some may still question if the plan’s funded status can really be maintained, especially after a year like 2020 with extreme volatility in the first quarter. The effects of plan expenses, credit migration and periodic actuarial adjustments can create drag on funded status, so what has been the actual experience for plans in hibernation?

In the exhibit below, we show the actual experience of three plans that adopted a hibernation as they approached a fully funded position. Each plan had an asset allocation containing 85%+ in high quality fixed income and reallocated these LDI assets every year based on updated actuarial cash flows and the current market environment. This is standard practice for any of our clients in hibernation.

In the lower two lines, you’ll notice they adopted their hibernation asset allocation even before they were fully funded. None of these sponsors made any contributions over the horizon, and plan expenses (including PBGC premiums, actuarial fees and investment management fees) were paid from plan assets.

Evolution of funded status

12/31/2016 – 12/31/2020

For each of these plans, the funded status has been steady over time. Note that despite multiple periods where funded status was severely challenged in the DB industry at large, the funded status of these plans have remained fairly consistent. Ironically, funded status actually increased in Q1 2020 during the recent COVID-related turmoil. These are just three actual examples of how the hibernation strategy can work if properly executed.

Common concerns with hibernation

Some may question of the merits of hibernation on the following grounds. We’d like to address each of them.

PV of future expenses: some argue that the present value of future expenses required by DB plans justifies paying an additional premium to an insurance company to annuitize the plan. However, if the plan assets generate sufficient return to compensate for these expenses directly (as our real life examples demonstrate), the sponsor will not be required to make contributions to cover them.

Credit migration: we have demonstrated repeatedly with our clients that the effects of defaults and downgrades can be significantly reduced through an effective LDI strategy and composition, alongside skilled investment management.

Actuarial gains/losses: plan hibernation is not designed to directly hedge against actuarial losses. Actuarial valuations should be unbiased and thus lead to similar potential for actuarial gains as much as losses, but a sponsor can only hedge this risk completely through insurance products. For this reason, we typically advocate building in a small funded status buffer above accounting liability at the outset of hibernation to help protect funded status in the case that assumptions used by the plan’s actuary are not aligned with future experience. Nevertheless, even if the funded status is impacted by such actuarial losses over the short term, contributions are unlikely to be required under current funding rules, allowing time for the funded status to recover.

Of course, while our actual client experience with hibernation strategies has been positive, other sponsors that are unable or unwilling to take any of these risks may deem the insurance premium required for full plan termination to be worth the expense. But the majority of plan sponsors appreciate the flexibility plan hibernation offers, until the financial and administrative timing of full plan termination is appropriate.

Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Russell Investments is the owner of the trademarks, service marks, and copyrights related to its respective indexes. Investments in products based on the Russell indexes may not provide the exact performance of the index due to implementation strategies, expenses and fees applicable to the investment product.

The Russell Investments logo is a trademark and service mark of Russell Investments.

AI-28684