InvestNow News – 31st July – Russell Investments – How you can turn risk in your favour

Article written by Russell Investments – 25th June

Mention the word ‘risk’ when talking about investments and most people instinctively think you are talking about the possibility of losing money. This is an important consideration, but there is a lot more involved in understanding the risks surrounding investments. And it’s not all bad news. For example, did you know you can turn risk to your advantage and profit by it?

The COVID-19 outbreak has re-introduced volatility and uncertainty back into the financial markets. For the first time in a long time, investors have been reminded about the realities of investment risk and potential loss. In these turbulent times, it is important for investors to put aside emotions, concentrate on their overall financial objectives and stick to a clear long-term financial plan.

Financial risk is relevant to everyone, regardless of how much money we have to invest. Every time we choose how to spend our money – no matter how small an amount – we are making an investment decision. Buying a house is an investment decision, as are depositing your pay into a bank account, buying some shares, or putting a few coins into a piggy bank. There are various types of investment risk attached to every investment decision we make.

Rather than labelling all risk as “bad” and something to avoid at all costs, consider that, realistically, accepting some form of risk is an essential element in helping your investments produce desirable long-term returns. As we shall see, you cannot completely avoid risk anyway (even a humble deposit in a bank account faces risks), so if you can’t eliminate it, you may as well understand it and use it to your advantage.

Six faces of investment risk

1. Asset class risk

Asset class risk refers to the possibility that the performance of a particular asset class could differ from another asset class. While each asset class is exposed to various risk factors, some asset classes are naturally more volatile than others. You can think of volatility as a measure of return dispersion i.e. the higher the volatility, the higher the risk of not achieving a consistent or expected level of returns from period to period.

Some investors aim to avoid volatility, and mistakenly think they are also avoiding risk, by investing primarily in cash. However, over the long-term, the risk of underperformance by investing in cash is virtually guaranteed and can result in a failure to achieve your financial objectives. The returns generated by cash are typically 3-4% per annum lower than those generated by shares over long horizons.

2. Active management (or benchmark) risk

A benchmark is a selected measure (usually a market index) chosen for the purpose of comparing results. For example, we may choose the NZX50 Index as a benchmark against which we can compare the returns of various NZ share funds

Investors are interested in benchmark risk because they are faced with the choice of:

- a passive fund manager who charges minimal fees and aims to provide a return equal to a nominated benchmark return. Hence, there being minimal benchmark risk when investing with a passive fund manager.

- investing with an active fund manager, whose fees are higher than those of passive managers, but who aims to provide a return above the benchmark. Investing with an active manager means benchmark risk is higher but in return, investors gain the opportunity of achieving above benchmark returns.

When investors place their money with an active manager they are essentially betting on the skill of that manager. There is an expectation that an investment will perform better than the benchmark, however, there is a corresponding risk that higher returns will not be achieved.

The further an active manager deviates from investing in a portfolio that matches the benchmark, the greater the benchmark risk. Benchmark risk is not a bad thing; for an active manager to achieve above-benchmark returns it must deviate from the benchmark portfolio and have convictions about certain stocks (overweighting in shares it believes will perform well and underweighting in those it believes will not).

3. Interest rate risk

Interest rate risk affects different securities and asset classes differently. When interest rates rise, financial securities lose value. Interest rate risk is usually most relevant to bond securities.

When new securities are issued at a higher interest rate than existing securities, existing securities lose value. For example, consider Bond A: a $10,000 government bond that pays 3% a year (priced at par value). If interest rates increase to 3.25% next month, why would anyone buy Bond A at $10,000, when the government is now issuing $10,000 of Bond B that pay 3.25% a year? If interest rates fall, existing securities on higher rates are immediately worth more, and vice versa.

While rising interest rates increase the cost of doing business for most companies (as the cost of borrowing increases), some companies and industries, such as banks, benefit from rising rates. Rising interest rates also affect residential property investors. As interest rates rise, so do investors’ loan repayments.

4. Inflation risk

Inflation erodes the buying power of our money and reduces the value of our income and savings. Inflation risk is particularly relevant for those people who invest most or all their money into cash and fixed interest investments.

If you have any doubt as to the large impact that inflation has on your investments, consider the following examples. In the 2019 calendar year, an investment into New Zealand cash would have returned approximately 1.7%1. Allowing for a tax rate of, 28% leaves you with a 1.2% after-tax return. The impact of inflation in New Zealand was 1.9%2 for the same period, which is higher than the after-tax return. An investment in cash in 2019 therefore results in a negative after-tax real return.

5. Currency or exchange risk

Investments in international assets are affected by fluctuations in currency values. A ‘strong’ Kiwi dollar can buy more foreign goods, including international shares. If the Kiwi dollar falls in relation to other currencies, the value of our international investments automatically rises (even though their price in local dollar terms hasn’t changed) as more of our ‘weak’ Kiwi dollars are now needed to buy the same amount of those foreign shares.

It is also worth noting that many New Zealand companies earn revenues in other countries in their respective currencies and might benefit from a falling New Zealand dollar.

6. Timing risk

The fear of losing money has caused many investors to attempt to manage returns by timing the market. That is, trying to work out how certain asset sectors will perform in the short-term and then buying or selling accordingly. Russell research has shown that no-one, even professional investors, can correctly time the market on a continual basis. Individual investors are notorious for timing trades incorrectly, buying in droves in the excitement of market highs and selling in droves in the despair of market lows.

Investors that focus on short-term fluctuations are more likely to make irrational investment decisions. The fear of losing money can cause them to shift out of more volatile investments, such as shares, to perceived safer holdings, such as cash trusts, or perhaps sell up their investments altogether. In attempts to reduce performance anxiety, many investors open themselves up to market timing risk by selling low and locking in losses and subsequently missing opportunities for growth when the market rebounds.

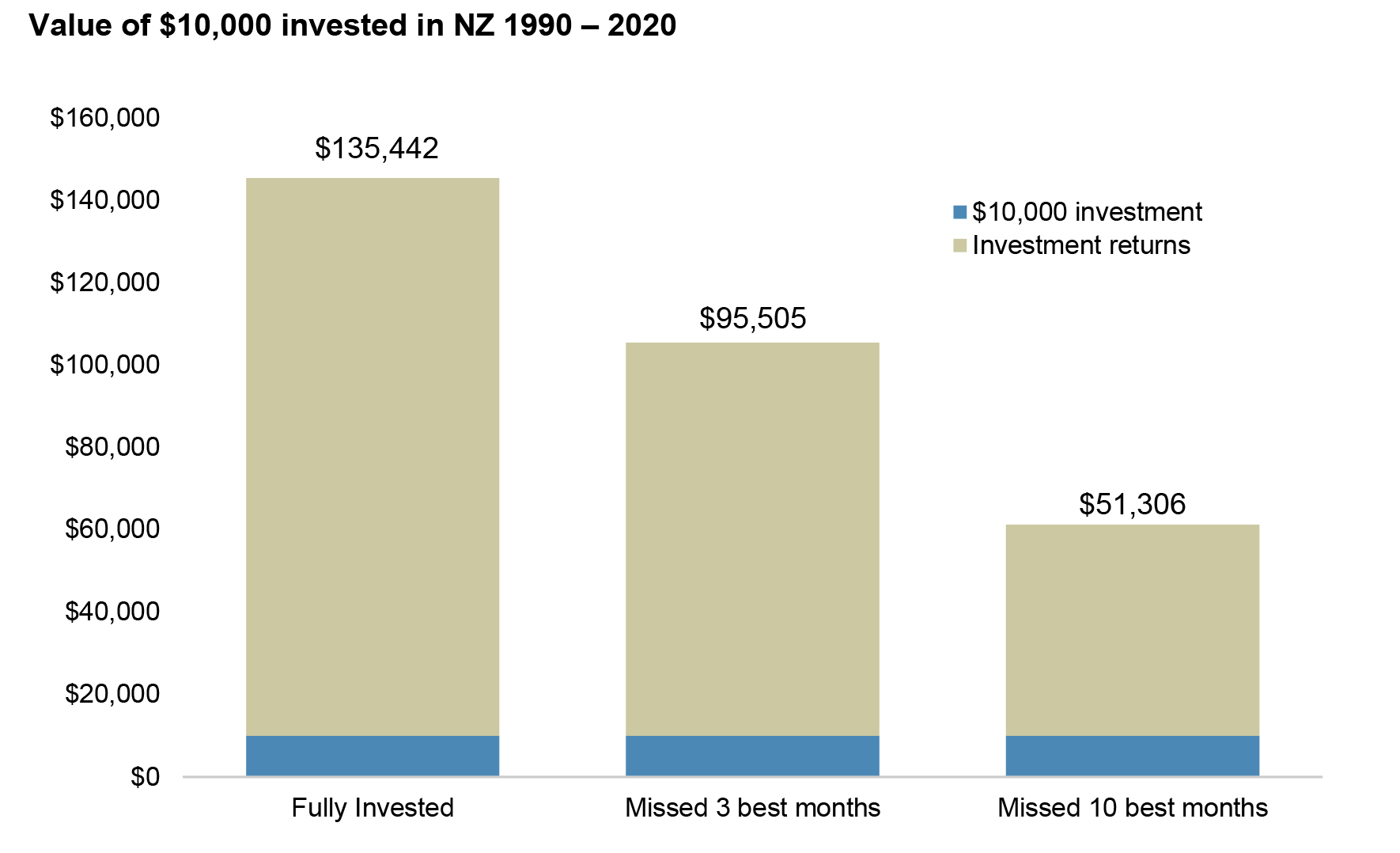

The importance of being disciplined, sticking to your plan and staying invested over the long-term cannot be underplayed. If you were fully invested in New Zealand shares since June 1990, a $10,000 investment would have been worth $135,442 at the end of May 2020 – an annualised return of 9.1%. If you missed the three best months during this 30-year period, your investment would be worth significantly less, round $95,505. If you missed the ten best months of the market over this 30-year period, your investment would now be worth $51,306. This stark difference reflects the importance of avoiding panic during market volatility.

1 NZX 90-day bank bill index.

2 Reserve bank of New Zealand

InvestNow News – 31st July – Russell Investments – How you can turn risk in your favour

Article written by Russell Investments – 25th June

Mention the word ‘risk’ when talking about investments and most people instinctively think you are talking about the possibility of losing money. This is an important consideration, but there is a lot more involved in understanding the risks surrounding investments. And it’s not all bad news. For example, did you know you can turn risk to your advantage and profit by it?

The COVID-19 outbreak has re-introduced volatility and uncertainty back into the financial markets. For the first time in a long time, investors have been reminded about the realities of investment risk and potential loss. In these turbulent times, it is important for investors to put aside emotions, concentrate on their overall financial objectives and stick to a clear long-term financial plan.

Financial risk is relevant to everyone, regardless of how much money we have to invest. Every time we choose how to spend our money – no matter how small an amount – we are making an investment decision. Buying a house is an investment decision, as are depositing your pay into a bank account, buying some shares, or putting a few coins into a piggy bank. There are various types of investment risk attached to every investment decision we make.

Rather than labelling all risk as “bad” and something to avoid at all costs, consider that, realistically, accepting some form of risk is an essential element in helping your investments produce desirable long-term returns. As we shall see, you cannot completely avoid risk anyway (even a humble deposit in a bank account faces risks), so if you can’t eliminate it, you may as well understand it and use it to your advantage.

Six faces of investment risk

1. Asset class risk

Asset class risk refers to the possibility that the performance of a particular asset class could differ from another asset class. While each asset class is exposed to various risk factors, some asset classes are naturally more volatile than others. You can think of volatility as a measure of return dispersion i.e. the higher the volatility, the higher the risk of not achieving a consistent or expected level of returns from period to period.

Some investors aim to avoid volatility, and mistakenly think they are also avoiding risk, by investing primarily in cash. However, over the long-term, the risk of underperformance by investing in cash is virtually guaranteed and can result in a failure to achieve your financial objectives. The returns generated by cash are typically 3-4% per annum lower than those generated by shares over long horizons.

2. Active management (or benchmark) risk

A benchmark is a selected measure (usually a market index) chosen for the purpose of comparing results. For example, we may choose the NZX50 Index as a benchmark against which we can compare the returns of various NZ share funds

Investors are interested in benchmark risk because they are faced with the choice of:

- a passive fund manager who charges minimal fees and aims to provide a return equal to a nominated benchmark return. Hence, there being minimal benchmark risk when investing with a passive fund manager.

- investing with an active fund manager, whose fees are higher than those of passive managers, but who aims to provide a return above the benchmark. Investing with an active manager means benchmark risk is higher but in return, investors gain the opportunity of achieving above benchmark returns.

When investors place their money with an active manager they are essentially betting on the skill of that manager. There is an expectation that an investment will perform better than the benchmark, however, there is a corresponding risk that higher returns will not be achieved.

The further an active manager deviates from investing in a portfolio that matches the benchmark, the greater the benchmark risk. Benchmark risk is not a bad thing; for an active manager to achieve above-benchmark returns it must deviate from the benchmark portfolio and have convictions about certain stocks (overweighting in shares it believes will perform well and underweighting in those it believes will not).

3. Interest rate risk

Interest rate risk affects different securities and asset classes differently. When interest rates rise, financial securities lose value. Interest rate risk is usually most relevant to bond securities.

When new securities are issued at a higher interest rate than existing securities, existing securities lose value. For example, consider Bond A: a $10,000 government bond that pays 3% a year (priced at par value). If interest rates increase to 3.25% next month, why would anyone buy Bond A at $10,000, when the government is now issuing $10,000 of Bond B that pay 3.25% a year? If interest rates fall, existing securities on higher rates are immediately worth more, and vice versa.

While rising interest rates increase the cost of doing business for most companies (as the cost of borrowing increases), some companies and industries, such as banks, benefit from rising rates. Rising interest rates also affect residential property investors. As interest rates rise, so do investors’ loan repayments.

4. Inflation risk

Inflation erodes the buying power of our money and reduces the value of our income and savings. Inflation risk is particularly relevant for those people who invest most or all their money into cash and fixed interest investments.

If you have any doubt as to the large impact that inflation has on your investments, consider the following examples. In the 2019 calendar year, an investment into New Zealand cash would have returned approximately 1.7%1. Allowing for a tax rate of, 28% leaves you with a 1.2% after-tax return. The impact of inflation in New Zealand was 1.9%2 for the same period, which is higher than the after-tax return. An investment in cash in 2019 therefore results in a negative after-tax real return.

5. Currency or exchange risk

Investments in international assets are affected by fluctuations in currency values. A ‘strong’ Kiwi dollar can buy more foreign goods, including international shares. If the Kiwi dollar falls in relation to other currencies, the value of our international investments automatically rises (even though their price in local dollar terms hasn’t changed) as more of our ‘weak’ Kiwi dollars are now needed to buy the same amount of those foreign shares.

It is also worth noting that many New Zealand companies earn revenues in other countries in their respective currencies and might benefit from a falling New Zealand dollar.

6. Timing risk

The fear of losing money has caused many investors to attempt to manage returns by timing the market. That is, trying to work out how certain asset sectors will perform in the short-term and then buying or selling accordingly. Russell research has shown that no-one, even professional investors, can correctly time the market on a continual basis. Individual investors are notorious for timing trades incorrectly, buying in droves in the excitement of market highs and selling in droves in the despair of market lows.

Investors that focus on short-term fluctuations are more likely to make irrational investment decisions. The fear of losing money can cause them to shift out of more volatile investments, such as shares, to perceived safer holdings, such as cash trusts, or perhaps sell up their investments altogether. In attempts to reduce performance anxiety, many investors open themselves up to market timing risk by selling low and locking in losses and subsequently missing opportunities for growth when the market rebounds.

The importance of being disciplined, sticking to your plan and staying invested over the long-term cannot be underplayed. If you were fully invested in New Zealand shares since June 1990, a $10,000 investment would have been worth $135,442 at the end of May 2020 – an annualised return of 9.1%. If you missed the three best months during this 30-year period, your investment would be worth significantly less, round $95,505. If you missed the ten best months of the market over this 30-year period, your investment would now be worth $51,306. This stark difference reflects the importance of avoiding panic during market volatility.

1 NZX 90-day bank bill index.

2 Reserve bank of New Zealand